5 apps to get your Coronavirus budget in shape

COVID-19 has upended how people in Australia and around the world work and live. Most of us are working from home, may have reduced income, or could be dealing with redundancy – one way or another, we're adjusting to new financial realities. For those who still have plenty of work and a high income, the reduced spending that comes with iso life is an opportunity to put money towards your long-term goals.

Economic uncertainty ahead

While the government’s economic stimulus packages will help right now, it's impossible to predict how the real economy will bounce back in the medium-term. So now is the time to review your spending and tweak your budget in line with those new realities. Eliminating expenses you don’t truly need and directing any excess cash to your savings or mortgage will give you some wriggle-room as you navigate through the uncertainty ahead.

Spending is more invisible

Tap and go, AfterPay, multiple credit cards and rewards programmes can all make it hard to keep track of expenses as our spending becomes increasingly invisible. One thing we can still do in lockdown is shop online and it's easy for those credit card charges to stack up without even leaving the couch.

And it's not just young people in the early stage of their careers that can fail to achieve their goals through careless budgeting. Successful professionals or business owners in their 30s or 40s often find their income growing rapidly over a short time as a direct result of their success, and their lifestyle and expenses quickly rise too. I've had this conversation with many successful people who earn great money, but feel like they aren't where they wanted to be financially. If this rings true for you, now is the perfect time to reset your budget.

Income is your greatest asset

Consider what is really important to your happiness now and in the future. Do you need two cars on lease, can you cut-back on outsourced services and with overseas travel plans on hold for now, can more money be directed to superannuation or other assets? As an adviser, I know high-income earners can only build wealth if they treat their income like an asset and invest it for greater returns. Ultimately that means spending wisely to free up funds to achieve your medium and long-term goals.

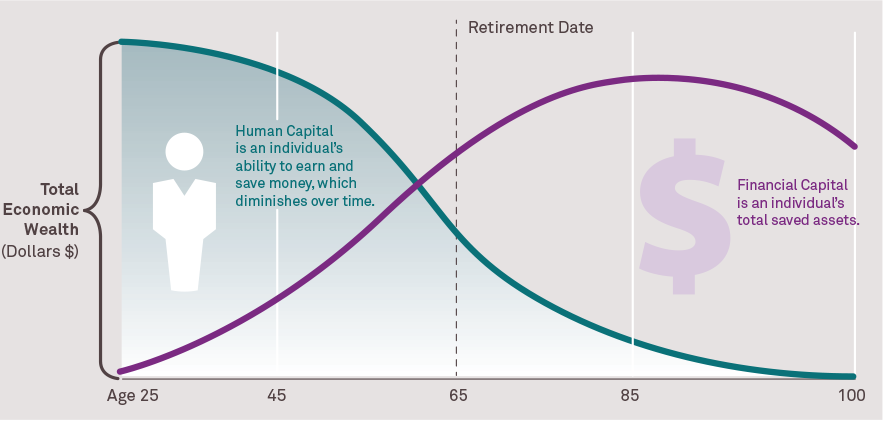

The below chart shows the importance of converting income earned throughout your career (human capital) into long-term wealth (financial capital), something our proven advice process is designed to help you achieve.

Budgeting is good for relationships too

Often couples budget well in their early years when money is tight, but as they achieve success and income grows, their spending becomes more relaxed. Just having the discussion can bring couples closer together on what they want to achieve from their shared financial success.

Control your spending to thrive

There are numerous online tools and apps available to take the pain out of budgeting and a lot can be automated. From categorising expenditure to handling multiple bank accounts and keeping track of your savings and investments, these apps are designed to make coordinating personal and business finances easier. The process of trialling one of these apps can help you get more deliberate about how much of your hard-earned income you want to spend and whether you're getting enough of a return.

The below technologies can help you get started. Once you've done your research on the best option for your needs, you can use their online portals or download the apps from the App Store for iPhone or Google Play for Android.

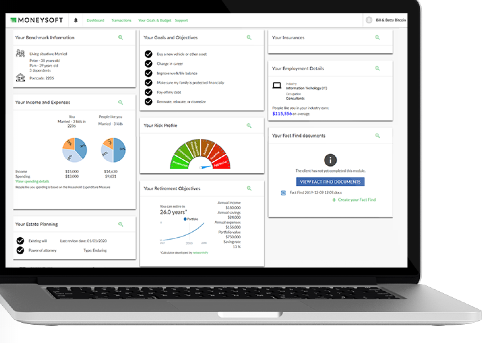

1. Moneysoft

An FMD partner, Moneysoft solutions support the adviser-client relationship and help make achieving clients’ financial goals a shared responsibility. Cash flow, budgeting, saving and goal-tracking are all available through their user-friendly platforms, supported by a single dynamic view of financial data. There is also a personal product where those not currently under advice can use the Moneysoft online financial management tool to brings together all their financial data, from multiple accounts and different locations, into one easy-to-use view of their finances.

Visit for more https://www.moneysoft.com.au/personal/ information.

Great for: Quickly and easily understanding your family spending

Shortcomings: The app is not yet as good as the online experience

2. Pocketbook

The free app syncs with most local banks making it easier to transfer your account information for accurate on-the-go budgeting. If you pay your bills via your online bank account, Pocketbook will alert you to overdue expenses, as well as send you weekly budget summaries.

Visit getpocketbook.com for more information.

Great for: Personal budgeting

Shortcomings: If you're with a smaller bank or neo bank, it may not be supported in the app's syncing feature. This will require you to add in your information manually.

3. Money Brilliant

With MoneyBrilliant, you can connect bank accounts, credit cards, loans, superannuation and more, in a single location. While the 'Basic' plan is free, the app also has a 'Plus' plan which gives you access to features such as the tax tool which can help identify tax-deductible transactions, an Insurance Tracking tool, and Bill Watch for good deals on electricity and gas bills.

Visit www.moneybrilliant.com.au for more information.

Great for: A comprehensive look at your finances

Shortcomings: Some great features are only available through the Plus (paid) plan

4. YNAB

You Need A Budget, or YNAB, is built on four rules of budgeting, one being 'zero-based budgeting,' a method in which all expenses must be justified and approved for each new period. The app lets you set and track goals and sends reports showing your progress. YNAB also offers a financial support team and budgeting workshops for a highly controlled approach to managing your budget designed to change spending behaviour.

Visit youneedabudget.com for more information.

Great for: Getting spending and debt under control to achieve your savings goal.

Shortcomings: There is no free version of this app (but it delivers more support than some of the free options)

5. Your bank's app

While it's common amongst digital and neobanks, many of Australia’s major banks have also jumped on board to create apps that help their customers with their saving goals. Your bank’s mobile app may have tools for budgeting, categorising expenditure, paying bills and more.

Great for: Security. You don't have to share your bank details with another app

Shortcomings: You can't connect to multiple bank accounts

The bottom line?

Dealing with anxiety around money and COVID-19 is still quite new territory for everyone. By controlling our spending, we can alleviate some of that anxiety and refocus our energy on our future goals, health and wellbeing.

If you'd like to discuss your financial goals in more detail, please contact one of our advisers.

Have questions about budgeting?

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.