Property Market Outlook

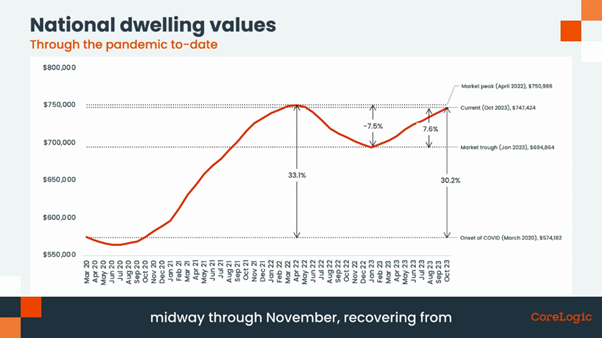

Despite rising interest rates, the low availability of housing stock and demand for residential property has seen steady price growth across capital city markets in 2023, as the below chart from Core Logic’s National Dwelling Value Index shows.

As more listings have come on to the market in spring, there is concern among some commentators that the pace of growth may slow, if weaker consumer demand can’t keep up.

In a sign that borrowing constraints from higher interest rates are biting, auction clearance rates have slowed from the low 70% mark in May to the low 60% mark in October.

The outlook for house prices

The FMD Investment Committee believes this is largely a temporary factor and that market fundamentals will keep most housing markets robust in 2024, provided interest rates rises don’t keep tracking higher.

David McMillan, Director at Performance Property, agrees.

“The macro outlook for 2024 shows undersupply everywhere and rents rising aggressively. Rents are up 75% in the last three years in Perth alone, says David.

“The market is pricing in cash rates coming down in 2024 and we’re expecting the median house price in Melbourne, currently at $850,000, to reach $1 million.

That’s why we recommend holding houses in Melbourne until there is more certainty around the outlook for interest rates.”

The outlook for unit prices

According to David, when it comes to unit prices, after a decade or more of stagnation, growth is anticipated across almost all markets, as rental demand continues to outstrip supply.

Of course, anyone with a variable mortgage is going to feel the pressure of rising interest rates taking a greater share of income, and people coming off low fixed rates will really feel the pinch.

The real winners are those who have already paid off rental properties and are now reaping the rewards of record-high rents without the higher loan servicing costs

Good news for downsizers

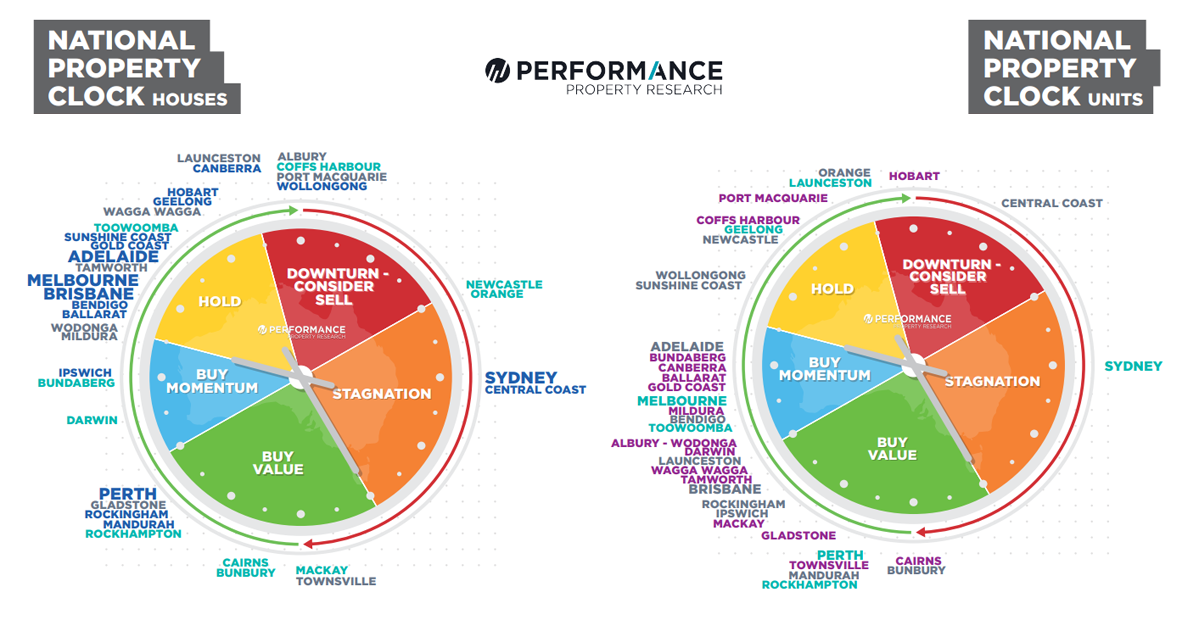

The below property clocks show that in many markets, 2024 could be a good time to downsize with further growth expected in house prices and strong value and buy momentum in units.

The best timing will again depend on what happens with interest rates, and in which markets you sell a house and then buy a unit.

Where these fundamentals are right, combined with Government downsizer incentives that enable people to put significant sums from the proceeds of a home sale into superannuation, downsizing could be a great move, both financially and from a lifestyle perspective.

If you have any questions about upcoming property investment decisions, please talk with your FMD adviser.

For more complex property portfolio management and advice, your adviser can also put you in touch with the team at Performance Property.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.