Markets rebound as earnings lift

Markets rebounded strongly in April after the sharp volatility seen in March. While geopolitical tensions in the Middle East continued and oil prices remained elevated, investors became more optimistic, focusing on resilient company earnings and the possibility that the conflict may ease.

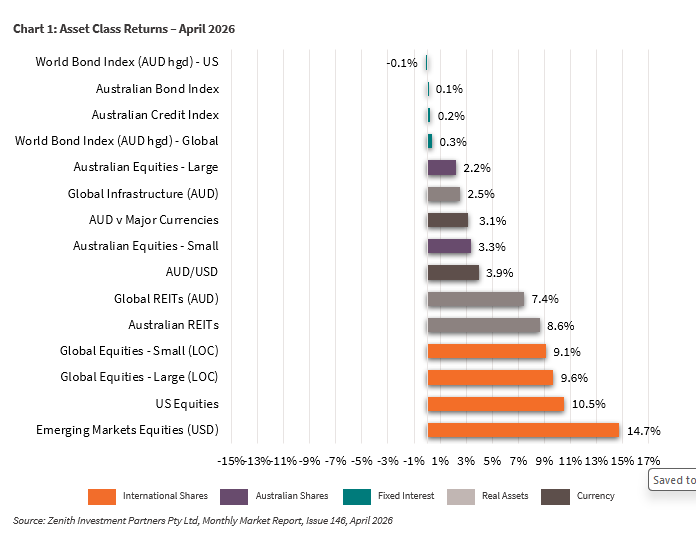

Global equities led the recovery, particularly technology stocks, as enthusiasm for artificial intelligence (AI) and strong earnings from major US companies drove gains. Emerging markets also bounced back sharply after the prior month’s sell-off.

Inflation remains a key theme for markets. Price pressures are still elevated, driven in part by higher fuel costs, and this is keeping central banks cautious. Interest rates are now expected to remain higher for longer, with some economies even facing further rate rises.

In Australia, the Reserve Bank continues to take a firm stance on inflation, lifting rates again and signalling more tightening may be required.

Overall, April showed that markets can recover quickly when confidence returns, but the underlying challenges of inflation, interest rates and geopolitical risks remain firmly in place.

Global Developed Equities

Global developed markets staged a strong recovery in April, with the MSCI World ex Australia index rising around 9–10% in US dollar terms for the month. This rebound reflected a shift in investor sentiment, as markets looked beyond geopolitical risks and focused on strong corporate earnings and growth opportunities.

The rally was led by technology stocks, particularly companies tied to AI development. Semiconductor businesses and large technology firms delivered strong earnings results, with many exceeding expectations.

US equities were particularly strong, with the S&P 500 rising over 10% to reach new highs, supported by earnings growth of more than 25% year-on-year. Notably, a high proportion of companies beat earnings forecasts, reinforcing confidence in the sector.

Other sectors also participated, though to a somewhat lesser extent. Financials performed solidly, while energy stocks pulled back slightly after strong gains in March. Growth stocks outperformed value in April, reversing some of the earlier trend.

Despite strong market performance, inflation remains elevated, with US core inflation sitting above target. At the same time, economic activity remains resilient, supported by business investment, particularly in AI-related spending.

Looking ahead, markets are balancing strong earnings growth with ongoing inflation risks and uncertainty around central bank policy.

Australian Equities

Australian equities delivered a modest rebound in April, rising just over 2% for the month. However, they lagged global markets, reflecting a combination of higher interest rates and less exposure to the high-growth technology sector.

The Reserve Bank of Australia raised interest rates again in early May to 4.35%, reinforcing its focus on controlling inflation. Inflation has risen to over 4%, well above the target range, and is expected to remain elevated in the near term before gradually easing.

While economic activity remains relatively solid, both consumer and business confidence have weakened. The labour market is still tight, but rising interest rates are beginning to weigh on sentiment.

Company earnings have improved, particularly in the resources sector, supported by higher commodity prices. However, there have also been a number of profit downgrades, highlighting uneven conditions across the market.

Sector performance was mixed. Materials and technology performed relatively well over the year, while banks delivered modest gains and defensive sectors such as healthcare struggled. Mid-cap companies were particularly impacted by higher rates and concerns about technology disruption.

Overall, the Australian market remains supported by solid earnings but faces headwinds from higher interest rates and softer sentiment.

Emerging Markets

Emerging markets rebounded strongly in April, rising nearly 15% after a sharp decline in March. The recovery was driven by renewed investor interest in technology, particularly semiconductor companies linked to AI.

Markets such as Korea and Taiwan led the gains, with significant increases reflecting strong demand for chips and ongoing investment in AI infrastructure. Other regions also performed well, including India and Brazil, supported by improving economic conditions and, in some cases, lower interest rates.

The outlook for emerging markets remains broadly positive. Earnings growth is strong, and structural drivers such as rising consumer demand and improving financial stability continue to support the longer-term investment case.

However, risks remain in the short term. These include the potential escalation of geopolitical tensions, movements in oil prices and a strengthening US dollar, all of which can impact emerging economies.

Overall, while volatility remains, the underlying growth story for emerging markets is intact, particularly in areas linked to technology and commodities.

Property and Infrastructure

Property and infrastructure assets recovered in April after a difficult March. Global listed property rose around 7%, while Australian REITs also saw a strong rebound, though they remain weaker over the longer term.

The recovery was supported by stabilising bond yields, which had risen sharply in the previous month.

Infrastructure assets continued to perform steadily, benefiting from their ability to provide some protection against inflation.

While these sectors offer defensive characteristics and income potential, they remain sensitive to interest rate movements. As long as rates stay elevated, returns may remain uneven.

Fixed Interest – Global

Global bond markets remained under pressure in April, with yields rising further as inflation persisted and central banks signalled a willingness to keep policy tight. The US 10-year bond yield moved up to around 4.4%, reflecting higher inflation expectations.

Central banks are facing a difficult balancing act. Inflation remains above target, but there are concerns about the impact of higher rates on economic growth. As a result, markets are increasingly pricing in the possibility that interest rates may rise further rather than fall.

Credit markets showed some improvement, with spreads narrowing after widening in March. High yield bonds have delivered stronger returns over the past year compared to investment-grade bonds.

Overall, the outlook for fixed interest remains uncertain, with inflation and central bank policy continuing to drive market movements.

Fixed Interest – Australia

Australian bond markets were relatively flat in April, but yields remain elevated, reflecting ongoing inflation pressures and expectations of further rate increases. The 10-year government bond yield ended the month just above 5%.

The RBA’s continued tightening, combined with rising inflation, has challenged the traditional role of bonds as a defensive asset. Over the past year, returns have been modest to slightly negative.

Inflation has increased significantly, driven in part by higher fuel costs, and the economy appears to be running close to capacity. With slower productivity growth, even moderate demand can lead to price pressures.

Markets expect interest rates to peak around current levels, though some easing in expectations has occurred as growth is expected to slow in response to higher rates.

While higher yields improve long-term return potential, short-term volatility is likely to persist.

Commodities and Currencies

Commodity markets remained volatile in April. Oil prices eased slightly after the sharp rise in March but remained elevated due to ongoing supply concerns linked to the Middle East conflict. Prices fluctuated throughout the month, reflecting uncertainty around potential resolution.

Other commodities were mixed. Gold remained relatively stable, while iron ore continued to be supported by demand.

Currency markets saw a notable shift, with the Australian dollar strengthening strongly.

It rose above 72 US cents, supported by higher interest rates, firm commodity prices and improved risk sentiment. Other major currencies also gained modestly against the US dollar.

Overall, currencies and commodities are continuing to react to changing expectations around growth, inflation and central bank policy.

Key Takeaways for Investors

- Global markets remain resilient, supported by strong earnings, particularly in technology and AI-related sectors.

- Inflation is still elevated, keeping pressure on central banks and limiting the scope for rate cuts.

- Interest rates are likely to stay higher for longer, impacting both equity and bond markets.

- Geopolitical risks and oil price volatility remain key drivers of short-term market movements.

Bottom Line for Investors

Markets have shown they can recover quickly when confidence improves, but the underlying environment remains complex. Strong earnings growth—especially in technology—is supporting equities, while persistent inflation and higher interest rates continue to create headwinds. For investors, staying diversified and focused on long-term objectives remains essential as markets navigate this period of uncertainty and transition.

Looking for Personal Financial Advice?

This investment update is a general overview of market movements for the month. For personal financial advice to achieve your investment goals, contact your FMD adviser.

If you're new to FMD, but ready to get serious about planning your financial future or a worry-free retirement, book an initial discovery meeting with one of our financial advisers in Melbourne, Adelaide or Brisbane.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.