Economic Snapshot: Global growth holds firm

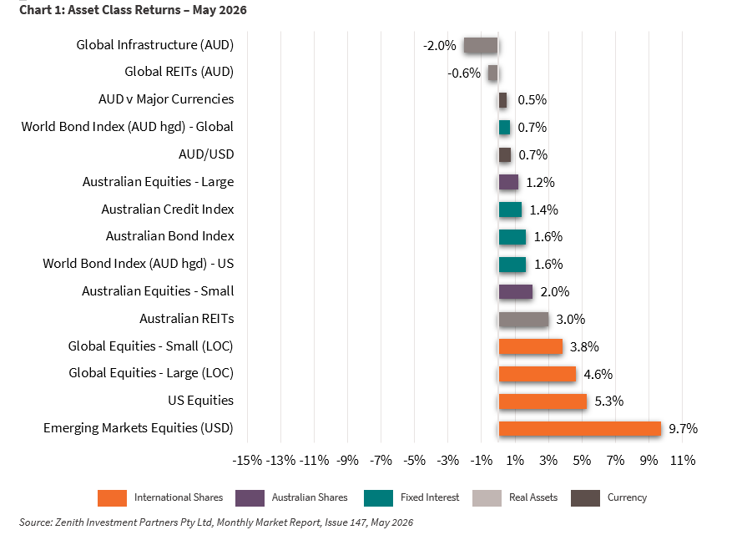

Global markets performed well in May, led by strong company earnings and continued momentum in artificial intelligence (AI) investment. Concerns about geopolitical tensions in the Middle East eased as oil prices fell later in the month, helping calm inflation fears and stabilise markets.

Technology and semiconductor companies remained the standout performers, as investors continued to back businesses benefiting from AI-related spending. Emerging markets also delivered strong returns, particularly in Asia where chipmakers drove growth.

In contrast, Australian equities lagged. This reflects both the market’s lower exposure to technology and a softer domestic economic backdrop, with higher interest rates weighing on growth.

Bond markets were volatile throughout the month. Early concerns about inflation and rising oil prices pushed yields higher, but softer economic data and easing energy prices helped markets recover toward the end of May.

Overall, the month highlighted a clear theme: strong global growth driven by innovation, alongside lingering uncertainty around inflation and interest rates.

Global Developed Equities

Global share markets continued their strong run, supported by better-than-expected corporate earnings and confidence that geopolitical risks would not significantly derail growth. AI-driven investment remains a powerful force, helping boost productivity and corporate profits.

Returns were strong, with global equities rising around 4.6% for the month and delivering more than 27% over the past year (in USD terms). The US and Japan led the gains, with technology stocks again playing a central role. In fact, tech has been one of the best-performing sectors this year, alongside energy.

Corporate earnings growth has been particularly strong in the US, with overall profits rising sharply, driven by large technology companies. Even so, valuations have not expanded significantly, as higher interest rate expectations have kept a lid on price multiples.

From an economic perspective, conditions remain reasonably supportive. Business activity is holding up, consumers are still spending, and government and corporate investment—especially in AI—continues to drive growth.

While inflation has ticked higher, longer-term expectations remain stable. This has reassured investors that central banks may not need to tighten policy aggressively from here.

Australian Equities

Australian shares delivered modest gains but continued to trail global markets. The key reason is structural: the Australian market has less exposure to high-growth technology companies and more exposure to sectors like financials and resources.

While resource stocks have performed well—supported by global demand and investment trends—other sectors have been weaker. Financials have been relatively subdued, and healthcare has experienced a significant decline over the past year.

The broader economic environment is also weighing on performance. Interest rates were increased again in May to 4.35%, as the Reserve Bank continues to manage inflation. Although headline inflation has eased slightly, underlying pressures remain elevated.

At the same time, economic momentum is slowing. Business and consumer confidence have weakened, and growth has been modest. Policy changes announced in the Federal Budget, particularly around property investment, have added uncertainty and may dampen both housing and broader economic activity.

Overall, Australia’s market is facing a combination of slower growth, higher interest rates, and less exposure to the sectors currently driving global returns. Overall, the Australian market remains supported by solid earnings but faces headwinds from higher interest rates and softer sentiment.

Emerging Markets

Emerging markets had another very strong month, driven largely by the global surge in demand for semiconductors and AI-related technologies. Returns were particularly strong in key Asian markets such as Korea and Taiwan, where major chip manufacturers are benefiting from this trend.

Over the past year, returns from emerging markets have been exceptionally strong, reflecting both earnings growth and investor enthusiasm for AI-driven sectors. However, this strength has been quite concentrated, with performance outside these key sectors and regions more subdued.

Some large markets, including China and India, have underperformed recently, while others like Brazil have lost momentum after earlier gains.

There are also some headwinds to consider. Rising US interest rates and a stronger US dollar can create pressure for emerging markets. That said, the global trade and manufacturing backdrop remains supportive, and improving fundamentals—such as healthier government balance sheets—offer a more positive long-term outlook.

Property and Infrastructure

Real estate and infrastructure investments lagged during the month as investors favoured higher-growth, riskier assets like technology stocks. Rising bond yields earlier in the month also weighed on these sectors, which tend to be more sensitive to interest rate movements.

Global real estate declined slightly in May but remains positive for the year. In Australia, real estate performed better, supported by exposure to data centres and improving bond market conditions toward the end of the month.

Infrastructure investments also fell modestly during May, although returns are still solid over the longer term.

Overall, these sectors remain more defensive and income-focused but have taken a back seat while growth-oriented assets have led the market.

Fixed Interest – Global

Global bond markets experienced a challenging and volatile month. Yields rose early on as inflation concerns resurfaced and central banks signalled the possibility of further interest rate increases.

In the US, bond yields moved higher as inflation picked up again and policymakers indicated they may need to tighten policy further if price pressures persist. Similar trends were seen in other major regions, with markets increasingly expecting potential rate hikes in Europe and Japan.

Despite this, conditions improved later in the month. Falling oil prices and softer economic data helped ease some inflation concerns and provided support for bond markets.Credit markets remained relatively stable, with stronger returns from higher-yielding bonds compared to more conservative investment-grade bonds over the past year.

Inflation and central bank policy settings continue to drive bond market movements. Benchmark yields are likely to remain volatile while markets assess the tension between persistent inflation pressures and the path of policy rates.

Fixed Interest – Australia

Australian bonds ended the month stronger after a volatile period. Yields rose earlier in May but fell back toward month-end as economic data pointed to a slowing economy and easing inflation pressures.

The Reserve Bank raised interest rates to 4.35%, citing ongoing inflation risks. However, subsequent data suggested some moderation, with inflation slowing and the labour market showing signs of softening.

Economic growth also appears to be losing momentum, reinforcing the idea that higher interest rates are starting to have an impact. At the same time, changes to fiscal policy have added uncertainty to the outlook for housing and consumer demand.

These factors combined to reduce expectations of further rate increases, supporting bond prices later in the month.In short, the Australian bond market is balancing two forces: inflation that remains above target, and a domestic economy that is beginning to slow.

Commodities and Currencies

Commodity markets were heavily influenced by geopolitical developments. Oil prices fell sharply as fears of prolonged supply disruptions eased, helping reduce inflation pressure globally. Gold remained elevated, supported by ongoing uncertainty, while iron ore held relatively steady on the back of resilient demand.

Currency movements reflected a mix of interest rate expectations and shifting market sentiment. The US dollar remained supported by relatively high interest rates, while the Australian dollar benefited from the recent rate hike and firm commodity prices, although gains were moderated by concerns about domestic growth and China’s outlook.

Overall, both commodities and currencies were responsive to changing expectations around growth, inflation, and central bank policy.

Key Takeaways for Investors

- Global equities remain strong, driven largely by AI-related growth and robust corporate earnings.

- Market leadership is narrow, with technology and semiconductor stocks dominating returns.

- Australian markets are lagging due to weaker growth and less exposure to high-growth sectors.

- Interest rates and inflation remain the key risks, driving volatility across both equities and bonds.

Bottom Line for Investors

Markets continue to be supported by strong earnings and long-term growth themes—particularly around AI—but this strength is coming with increased concentration and ongoing uncertainty.

While global growth remains resilient, higher interest rates and slowing economic momentum, especially in Australia, suggest a more uneven path ahead. Staying diversified and focusing on long-term fundamentals remains key in navigating this environment.

Looking for Personal Financial Advice?

This investment update is a general overview of market movements for the month. For personal financial advice to achieve your investment goals, contact your FMD adviser.

If you're new to FMD, but ready to get serious about planning your financial future or a worry-free retirement, book an initial discovery meeting with one of our financial advisers in Melbourne, Adelaide or Brisbane.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.