Economic Snapshot: The impact of COVID-19 on national and global economies - February 2020

Summary

The first three weeks of February saw further good performance by global equity markets. The news from China about COVID-19 seemed to be getting better and the latest economic data was still quite positive. However, all this changed very quickly from 21 February when markets suddenly became alarmed by reports of the virus spreading to several countries around the world, including Italy, Iran, South Korea and the US.

These developments reignited fears of global recession seen last year, and equity markets fell sharply, as did the price of oil and the A$, which ended the month at US0.652. Bonds rallied as equities fell. The US 10-year government bond yield dropped to a new record low around 1.15%, and the Australian equivalent yield falling to 0.84%. Gold initially rallied, but then gave up all its gains at the very end of the month as traders took profits in order to pay margin calls on other assets.

The big question is where to from here with these developments? We are moving into a phase where we will get more information about both COVID-19 and its impact on the global economy. There is a risk that the news flow gets worse before it gets better, but it will get better, though no-one knows exactly when.

In the meantime, central banks were in a wait-and-see mode. They didn’t want to act on interest rates until they better understood the scale of the problem. And, for now, the authorities in China are sticking with their policies of support rather than stimulus, for fear of reigniting the problems in their financial system they have been striving to fix.

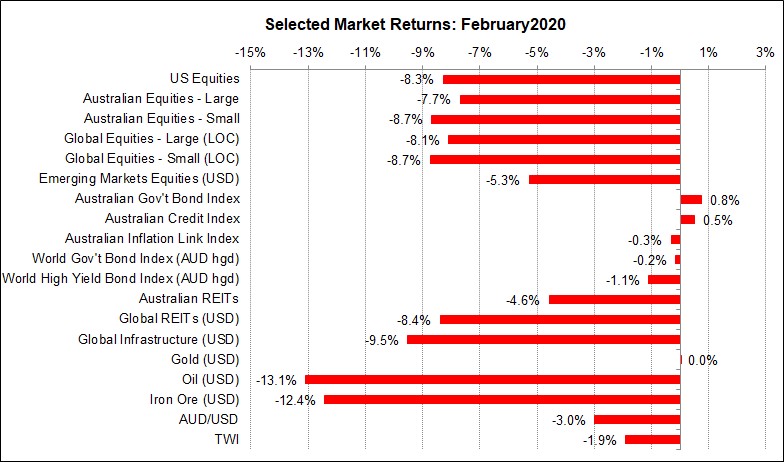

Figure 1: Spread of COVID-19 outside China hit global equity markets very hard

Source: Thomson Reuters, Bloomberg 1 March 2020

Global Financial Markets

The big developments in February involved the coronavirus, or COVID-19 as it is now officially designated. For most of the month financial markets largely took the virus in its stride. Infections were almost exclusively in China and official reports suggested the authorities were getting on top of things. Also, the economic data available at the time was yet to show the impact of the virus on key economic activity. Earnings reports from firms in both the US and Australia were close enough to expectations for the markets to be comfortable with the news. However, Apple waived a red flag when it said it would temporarily close 42 stores in China and later issued a sales warning based on the impact of the virus on the supply of its products.

To be sure, there was some less positive news, including from Japan where 2019 Q4 GDP came in much weaker than expected, raising fears the country may be more vulnerable to recession than previously thought. Here in Australia, the January Labour Force report showed both the unemployment and underemployment rates rising by 0.2% - 0.3% in January. Leading indicators continue to suggest the unemployment rate will edge up in coming months. Measures of local business confidence and conditions remained at subdued levels in January, as did measures of consumer confidence.

Impact of COVID-19

Overall, equity markets performed well in the first three weeks of February. The S&P 500 was up about 3.36% and the ASX200 was up 2%. In commodity markets, gold was up 3.5%, as was the price of oil, which had been hit quite sharply by COVID-19. The mood in the markets at this point was that COVID-19 would cut China’s growth in Q1 but that it would bounce back quickly in Q2 and therefore the markets could “look through” the temporary dip in growth and just keep going.

However, on 21 February the mood took a sharp turn for the worse. The catalyst for this was reports of the virus spreading around the world, including the death of some infected people. These reports included South Korea, Italy, Iran, Croatia and Spain which represented a broad enough geographic spread to surprise the markets. Italy and Spain present the risk of contagion spreading into France and Germany, the two big economies of Europe. Germany is already with weak growth induced by tighter economic policies implemented in China last year. Like Japan, Germany is not in a particularly strong position from which to be tackling COVID-19.

However, the markets were probably most disturbed by a warning from the US Centre for Disease Control and Prevention that it is not a matter of if, but when, the virus spreads across the country and that people should start preparing for this. This immediately led the markets to worry about a slowdown in the US economy and revived the recession fears that plagued markets last year.

Equity markets sold off very quickly, more than reversing their gains of earlier in the month. By the end of the month, the S&P500 was down 8.3%, and the ASX200 had fallen 7.7%. Other assets exposed to global growth also fell, with oil down 13.1% for the month and the A$/US falling 3% to US$0.652.

Bonds rallied as equities fell. The US 10-year government bond yield dropped to a new record low around 1.15%, and the Australian equivalent yield falling to 0.84%.

Where to from here?

The big question is where to from here with these developments? An important aspect of this is that we are moving into a phase where we will get more information about both COVID-19 and its impact on the global economy. Scientists outside China will be able to observe the virus firsthand, which will help give a clearer picture of how the virus operates and how the risk must be managed. Also, we will start getting economic data which will shed light on just how much trade and growth are being impacted. There is a risk that the news flow gets worse before it gets better, but it will get better, though no-one knows exactly when.

In the meantime, central banks and governments’ have begun to take action with many policy changes announced in mid-March. For now, the authorities in China are sticking with their policies of support rather than stimulus. That is, they will assist firms to survive the virus and get back to work, but they will not risk comprising progress to date on fixing bad debts and other problems in the financial system, which were created by too much stimulus in previous years.

Geo-political Activity

In other news, the US the Democratic Party primaries saw Bernie Sanders initially consolidate his lead over many of the other candidates, most of whom have faded as the primaries have progressed. Michael Bloomberg formally entered the race and was running second to Sanders, but he too had exited by the beginning of March. At the time of writing, Joe Biden holds the lead over Sanders, perhaps reflecting the sentiment that Sanders does not seem a safe choice. His policies are probably too radical for American voters and they are certainly anathema to Wall Street. Sanders as the Democratic candidate would make the markets very nervous.

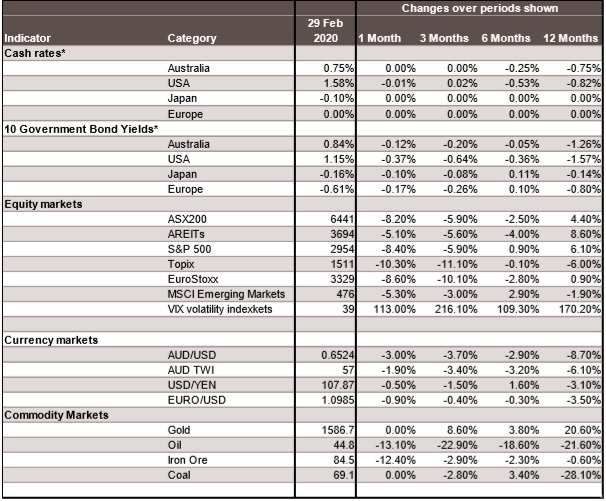

Figure 2: Major Market Indicators - February 2020

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.