Economic Snapshot: Rallying equities and early optimism - April 2020

Summary

Markets embraced a risk-on mood in April with a strong rally in equities as investors welcomed declining virus infections and reports of possible medical treatments. Support from governments and central banks also helped. However, as the month went on, the economic data and corporate reporting painted a bleaker picture of just how much damage has been done to the world economy. Markets have priced a lot of good news and now they are starting to see the bad news. Equity markets are looking expensive again after April’s rally, which does not leave much room for them to absorb bad news.

The other big development in April was in the oil market. Plagued by massive over-supply as the pandemic has crushed demand for oil, producers are running out of room to store the oil they are pumping out of the ground. On 20 April, the futures price of oil closed at –US$37 a barrel as producers were effectively prepared to pay buyers to take the oil off their hands. The oil market has never seen this before.

Government bond markets were relatively quiet in April, but credit and high yield markets rallied along with equities. The A$/US$ also participated in the risk-on mood, rising from US$0.612 at the start of April to US$0.657 at the end of the end of the month.

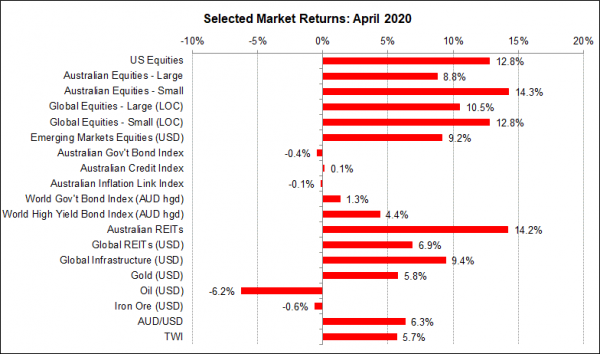

Chart 1: Equity markets bounced sharply in April, but oil fell.

Source: Thomson Reuters, Bloomberg 1 May 2020

Global Financial Markets

Equity markets rallied in April on hopes the pandemic would be brought under control sooner rather than later, thereby allowing a quicker re-opening of economies. Confidence in stimulus packages around the world encouraged the notion of a “V shaped” recovery and prompted further buying. Retail investors bought heavily, attracted by the prospect of significantly lower prices. Most of the rally occurred in the first half of the month, with momentum moderating in the second half. Even so, the S&P 500 recorded its best month in over 30 years.

COVID-19 Pandemic

There was some good progress on containing the pandemic in April. In most European countries the number of new cases per week fell steadily through the month as social distancing policies were enforced. However, the UK has not yet been able to establish the same profile of clearly moving past peak infections. China and Singapore saw second waves of infections but acted quickly to contain them. Australia has done very well in bringing the number of new cases per week down from 2,284 at the start of April to 92 by the end of the month.

The US has not yet made anywhere near enough progress on flattening the curve. New cases per week have been averaging around 200,000 and the total number of cases to end-April was just over 1 million, with 61,000 deaths. Despite this, pressure mounted through April to ease restrictions quickly, including some less than responsible comments from Mr Trump. At the same time, expectations were growing that a treatment, or even a vaccine, would be available sooner than expected. US drug company Gilead announced it had developed a treatment for the symptoms of the virus, though not a vaccine. The US FDA said it would fast track the drug for use on patients. Not surprisingly, equity markets took this as an excuse to rally further.

Unfortunately, the situation is more complex than this optimism might warrant. There are questions about the data behind Gilead’s trials as well as the ability to produce large volumes of the treatment. There are also concerns that the prospect of a medical solution is encouraging a population weary of social distancing to break free at a time when the infection rate is still dangerously high. The US is risking a major second wave of infections.

Economic Data

As April progressed, the economic data started to show just how bad the hit to the global economy is likely to be. For example:

- 30 million workers in the US filed for unemployment benefits in April;

- Figures from the Fed show US real GDP fell by 11.6% from its level a year earlier; this was three times worse than the lowest reading during the GFC;

- In many countries, measures of activity in both manufacturing and services collapsed to the lowest levels on record, with Europe especially hard hit;

- Data for Australia also show big falls in activity and employment;

- The IMF said the world is heading for the worst recession since the Depression, but that the downturn should be relatively short-lived.

This latter point is what the markets have been latching on to – the belief that once restrictions are eased people will quickly get back to work and spending the way they used to before the pandemic. This so-called “V shaped” recovery has been the popular view. However, the data are starting to suggest this may be overly optimistic:

- It is only now becoming clear just how big is the hole the world will have to climb out of, and the economic data will get worse in coming weeks;

- The deeper the hole, the longer will it take to get back where we were at the start of the year;

- Surveys in Australia, China and Europe show consumers are worried about losing their jobs and plan to save more rather than spend;

- Company earnings reports coming out around the world are showing significant damage to profits and dividends with the prospect of worse in coming months.

Although equity markets rallied strongly in April, these concerns started to bite at the end of the month with equities giving up some of their gains. Even so, the Australian and US equity markets have rallied enough to push their forward P/E (price/ earnings) ratios up into expensive territory. On this measure, the S&P500 is now more expensive than it was in February. There is little buffer for the markets to keep looking past more bad news.

Oil Market

The other big development in April was in the oil market. Plagued by massive over-supply as the pandemic has crushed the demand for oil, producers are running out of room to store the oil they are pumping out of the ground. Storage is so scarce there are fully laden tankers cruising the oceans or parked off the coast of countries which cannot offer them the means to unload their cargo.

On 20 April, the futures price of oil closed at –US$37 a barrel as producers were effectively prepared to pay buyers to take the oil off their hands. The oil market has never seen this before. Prices recovered to positive territory later in the week after Mr Trump said he ordered the US navy to fire upon Iranian vessels hindering US shipping in the Gulf. However, the oil market remains vulnerable to further price weakness. Shutdowns in activity across the industry in the US started in April, with nearly half the rigs operating in March being shut down in April.

Bond Markets

Government bond markets were relatively quiet in April, but credit and high yield markets rallied along with equities. The A$/US$ also participated in the risk-on mood, rising from US$0.612 at the start of April to US$0.657 at the end of the end of the month.

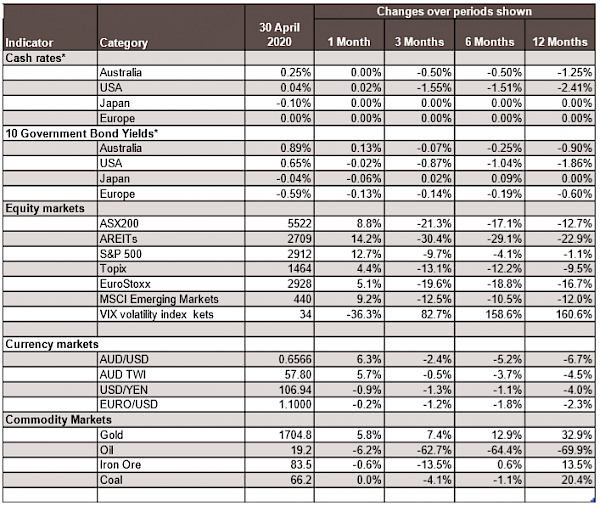

Chart 2: Major Market Indicators - April 2020

*For cash rates and bonds, the changes are % differences; for the rest of the table % changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.