Economic Snapshot: New COVID outbreaks slow growth

Summary

August saw more of the themes and risks that global financial markets had focused on in July. COVID-19 continued to spread around the world, leading to further slowing of economic activity, disruptions to global supply chains, and pockets of inflationary pressures.

Despite a weaker domestic economic outlook for the September quarter, the Reserve Bank of Australia decided to reduce its purchases of government securities by $1 billion a week from early September to a rate of $4 billion a week until at least mid-November.

The RBA also said it will not increase the cash rate until inflation is sustainably within the 2 to 3 per cent target range and that it does not expect that to happen before 2024. Importantly, the Reserve Bank Board separated tapering its bond purchases from when it would lift the cash rate. In the US, the Federal Reserve has said much the same thing.

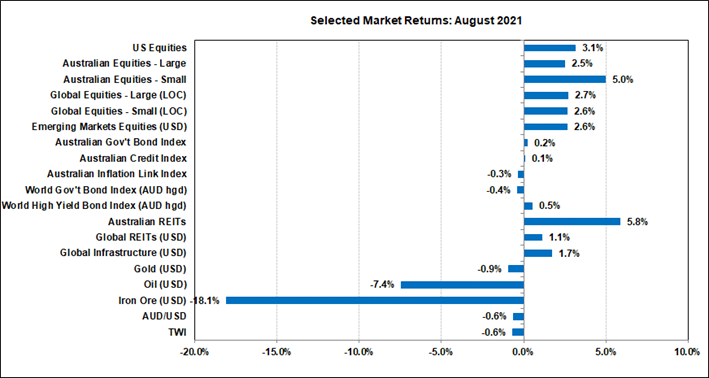

Nominal bond yields were little changed in August and most key equity market indices posted respectable gains for the month. Solid earnings reports helped the local and US equity markets reach new highs, but the ASX200 closed the month below those highs. Emerging markets remain an underperformer.

The A$/US$ exchange rate slipped towards US$0.71 before recovering a few cents by the end of the month as the US$ softened on reduced expectations of US interest rate increases. Gold slipped a bit more under the impact of slightly higher US real bond yields.

Chart 1: Gains in August 2021 helped push some equity markets to new highs

Source: Thomson Reuters, Bloomberg 1 September 2021

Overview

August saw more of the themes and risks that global financial markets had focused on in July. COVID-19 continued to spread around the world, leading to further slowing of economic activity, disruptions to global supply chains, and pockets of inflationary pressures. At the same time central banks continued to talk about winding back their bond-buying programs. Nevertheless, good earnings reports helped equity markets make new highs.

Covid-19

The delta variant of COVID-19 is proving every bit as contagious as feared. Here in Australia, weekly case numbers were around 1,300 at the end of July and around 7,400 by the end of August.

This compares with a peak around 3,750 cases per week in the second wave a year ago. Other countries are seeing similar escalations in case numbers, including the US, parts of Europe, Japan, and South Korea. Some countries are imposing lockdowns in response to these developments, but others are less inclined to do so as vaccination rates improve.

Supply Chain Interruptions

China was one of the countries which imposed strict lockdowns to contain the virus. While this has apparently been successful, it has also contributed to the disruption of global supply chains. For example, the closure of major port facilities and insufficient supply of container vessels has led to big increases in the cost of shipping freight around the world, as well as delays in getting that freight to its destinations.

Many manufacturers have moved from relying on just-in-time delivery to stockpiling inventories of key inputs. Even so, disruptions to production have led to higher prices for many goods, of which cars have been a well-publicised example. Labour markets have also been disrupted, with difficulty in finding workers because of COVID-19 restrictions leading to higher wages in some sectors.

Consumer Sentiment

Given all this, it is not surprising that financial markets have been wondering about higher inflation, but in August their attention was more on the risks to economic growth.

For example, latest figures illustrate the impact of the lockdowns in NSW and Victoria. Business Confidence fell again in July, to -7.9 from 10.6 the previous month.

This was the first negative reading for Business Confidence since September 2020. Business Conditions also declined sharply in July to 11.4 after 24.9 the previous month.

The Melbourne University/Westpac Consumer Sentiment index fell 4.4% in August, including higher expectations of unemployment. However, the full impact of the lockdowns on our labour market have yet to be felt. Employment rose slightly in July, and the unemployment rate fell to 4.6% from 4.9% the previous month.

Even so, the underemployment rate rose in July. It is now widely expected the September quarter will see negative GDP growth.

Monetary Policy

In this environment, central banks remain focussed on growth and unemployment rather than inflation. Indeed, they emphasised again that they see current inflationary pressures as transitory.

For now, the markets seem inclined to give them the benefit of the doubt. However, central banks are keen to start scaling back the degree of stimulus they have been providing to markets. To be clear, this does not mean the start of monetary tightening, just a moderation in the degree of stimulus by gradually reducing the volume of bonds they have been buying from the market. This operation is known as “tapering”.

Given the weaker economic outlook for Australia in Q3, economists and investors have been expecting the Reserve Bank to delay the start of its tapering, but at its meeting in early August the Board of the RBA decided to reduce its purchases of government securities by $1 billion a week from early September to a rate of $4 billion a week until at least mid-November.

The Board also said it will not increase the cash rate until inflation is sustainably within the 2 to 3 per cent target range and that it does not expect that to happen before 2024. Importantly, the Board separated tapering its bond purchases from when it would lift the cash rate.

USA

In the US, the Federal Reserve has done much the same thing. There has been much speculation about what the Fed would say after its annual Jackson Hole conference.

Markets are very keen to see that the Fed has learnt from its mistakes with tapering a few years ago. Fed Chair Jerome Powell also flagged a policy separating tapering from interest rate increases.

Markets expect an announcement about tapering in coming weeks. Several Fed Governors have expressed opinions about when interest rates should start to rise, but this largely focuses on late 2022 at the earliest.

Both the RBA and the Fed have flagged they will watch how the economic data unfolds and may adjust the pace of tapering as required.

Equities, Bonds, Commodities and Exchange Rates

Financial markets have taken all this in their stride and sentiment has improved as investors take heart from vaccination programs and start to look past the current COVID-19 wave.

Nominal bond yields were little changed in August and most key equity market indices posted respectable gains for the month. Solid earnings reports helped the local and US equity markets reach new highs, but the ASX200 closed the month below those highs.

Emerging markets remain an underperformer. The A$/US$ slipped towards US$0.71 before recovering a few cents by the end of the month as the US$ softened on reduced expectations of US interest rate increases. Gold slipped a bit more under the impact of higher US real bond yields.

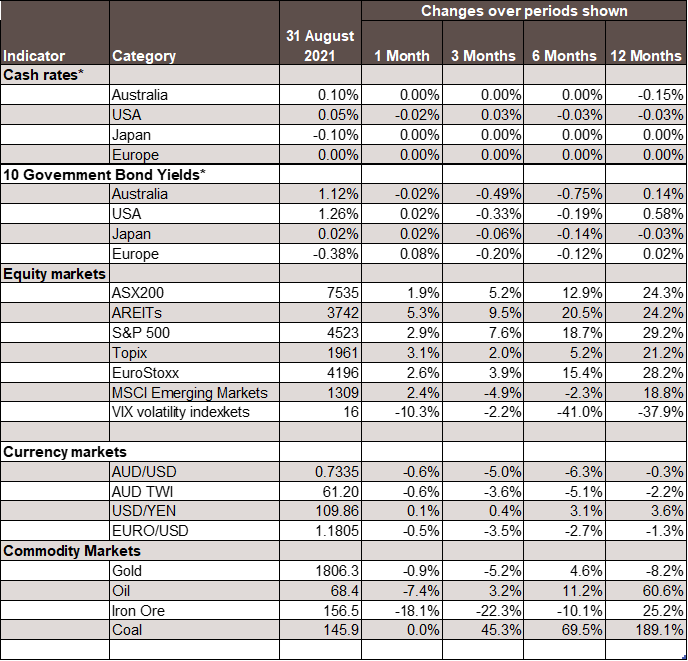

Chart 2: Major Market Indicators – August 2021

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.