Economic Snapshot: Markets take an optimistic turn - September 2019

Summary

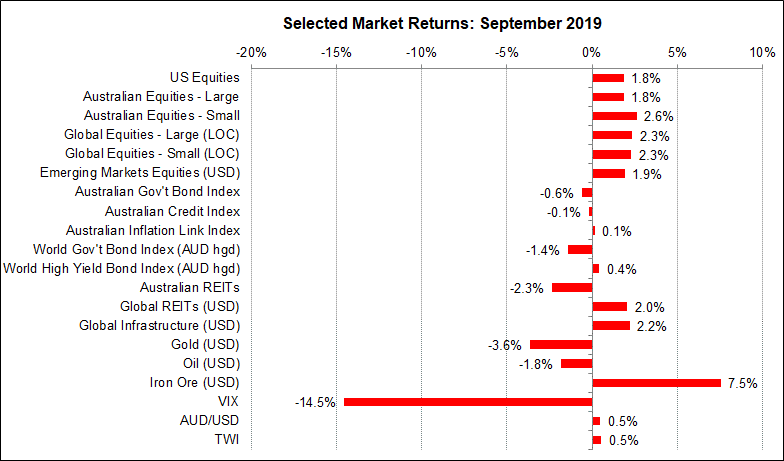

September’s market action was in clear contrast to the previous month. August’s concerns about global growth, trade wars and geopolitics gave way to a somewhat more optimistic mood in which the relative performance of key asset classes was reversed. In particular, equities rallied while bonds and gold sold-off in September.

The seasonal thinness of markets (overseas) improved in September as investors returned to work in time to take advantage of a more balanced news flow compared with the general negativity of the previous month. On the positive side, there were signs of a more conciliatory approach by both the US and China to the trade dispute, central banks around the world eased monetary policy, and the US economy posted more good data on employment and household spending. On the negative side, manufacturing activity around the world slipped further, adding to fears of recession, while a drone attack on Saudi oil fields caused a sharp, but transitory, spike in the price of oil.

Much of the price action between August and September simply cancelled itself out, leaving a bout of volatility in its wake. However, there is more to this than meets the eye, because the volatility reflects uncertainty, of which there is plenty in the world now, and not just on economic developments.

Geopolitical developments including Brexit, the move to impeach Trump, and increasingly violent protests in Hong Kong all contributed to the uncertainty.

Figure 1: September saw a reversal of the pessimistic sentiment and price action in August

Source: Thomson Reuters, Bloomberg 1 October 2019

Global Financial Markets

A key question preoccupying markets at the moment continues to be whether the world is sliding into a recession. Attention is focussed on the difference in performance between the manufacturing and service sectors around the world. Manufacturing has been hit hard this year by the slowdown in China and the impact of the trade dispute. The latest data shows Germany’s manufacturing sector, for example, is effectively already in a recession and the situation in the US seems to be heading in that direction.

In Australia, business conditions are still slipping. Weakness in export orders is a common factor driving the manufacturing slowdown. However, service sector activity has generally been better than manufacturing.

This makes sense since manufacturing produces a lot of internationally traded goods, while the output of the services sector tends to be consumed at home rather than abroad and so depends more heavily on local employment conditions. It is important to remember that the services sector in many developed economies, including the US, is larger than the manufacturing sector.

Trade Dispute and Manufacturing

The markets are increasingly concerned that, with no end in sight for the China/ US trade dispute, the weakness in manufacturing will spill over into the rest of the economy and tip it all into recession. Considering this, the markets are closely watching the Purchasing Managers Index (PMI) reports, employment data, retail sales and policy announcements from the major central banks. Most attention is focussed on the US, but the risks in Europe are becoming more pronounced.

Key data in released in September included:

- the US manufacturing PMI fell for the fifth month in a row to 49.1, below the key expansion/contraction level of 50, while the services PMI was 56.4;

- the composite PMI in the Eurozone fell to 50.4 in September from 51.9 in August, and in Germany the composite PMI fell to 49.1 in September, from 51.7 in August;

- US employment growth has slowed from last year’s pace, but is still strong enough to keep the unemployment rate around 3.7%; wages growth in the US has peaked and is slowing down;

- Australian GDP growth was weak in Q2 2019 (+0.5%) and just 1.4% over the year to the quarter; housing construction and consumption continued to be a drag on growth; public sector spending and net exports were the main drivers of growth in the quarter.

Monetary Policy – Interest Rates

Against this backdrop, there have been further moves to ease monetary policy. The US Federal Reserve cut the Federal funds rate target range by 0.25% to 1.75%-2.00% and said it would be ready to do more if necessary.

In Europe, the ECB announced a new stimulus package, including pushing interest rates further into negative territory and buying more bonds. However, the markets are not convinced the ECB can be very effective no matter what it does.

The Peoples Bank of China announced further cuts to bank reserve requirement ratios in order to boost lending, but the opaqueness of China’s financial system makes it hard to assess the effectiveness of the move.

Australia

Here in Australia, the Reserve Bank left the cash rate unchanged at 1.0% in September (note, the RBA did reduce rates by 0.25% at their early-October meeting), but markets still expect the RBA to cut to 0.5% by the end of the year. There has been increasing debate among commentators and market participants about how effective further interest rate cuts by the RBA can be at this stage, and speculation that the RBA will have to resort to “unusual measures” – that is, some form of quantitative easing - to achieve its objectives.

So far, the RBA has been coy about this, but in recent speeches they have made it clear they do not want the Australian dollar to appreciate. Given the RBA is running out of room to cut interest rates relative to the US, it is highly likely they will resort to intervening in the currency markets to sell the Australian dollar if necessary.

In September, the AUD/USD exchange rate traded in a range of US$0.67 – 0.69 for a net gain of 0.5% in the month.

Equity markets were pleased to see these moves by central banks in September, even if there were some reservations about their effectiveness. The main thing was that policy makers were not ignoring the signs of weaker global economic activity. This, plus some more encouraging signs about the US-China trade talks, helped equities to rally and bonds to retreat in September. But many uncertainties remain, so that further volatility should be expected in coming months.

Geopolitical developments:

Geo-political developments contributed to this climate in September:

- The (US) Democrats announced an impeachment inquiry into President Trump’s role in the “Ukraine affair”. It is far from clear if the Democrats will be successful, and even if they are in the House, where they control the numbers, they are unlikely to succeed in the Senate where they do not have the numbers;

- In the UK, things went from bad to worse for Boris Johnson seeking to deliver Brexit before 31 October. Not only did the Supreme Court rule his proroguing of Parliament to be unlawful, but further defections eliminated his Parliamentary majority. It seems more likely the UK will have a General Election before the year is out than a solution for Brexit;

- In Hong Kong, increasingly protests continued as demonstrators sought to keep the pressure on Xi Xingping ahead of the 70th anniversary celebrations in October; this situation does not look like ending anytime soon;

- A drone attack on Saudi oil fields caused enough damage to push the oil price up sharply on fears of reduced global supply. However, these concerns evaporated surprisingly quickly and the price of oil finished September nearly 2% down for the month.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.