Economic Snapshot: Energy shock reshapes markets

March was dominated by a sharp escalation in the Middle East conflict, which disrupted global oil supply and triggered a spike in energy prices.

That shock unsettled markets, as investors reassessed inflation risks and the likely path of interest rates. Share markets and bonds both fell, reversing some of the gains seen earlier in the year.

The rapid rise in oil prices raised concerns that inflation could remain higher for longer. As a result, central banks shifted from talking about possible rate cuts to signalling a willingness to raise rates further if needed. This change in expectations pushed bond yields higher and weighed on growth sensitive assets.

In Australia, the Reserve Bank lifted interest rates again, citing inflation that remains well above target. Globally, markets became more cautious, favouring defensive assets and currencies seen as “safe havens”.

While there is little evidence yet that the conflict has materially damaged economic growth, prolonged uncertainty and elevated oil prices would increase the risks to both growth and inflation.

Overall, March highlighted how quickly markets can change direction when geopolitical risks spill over into inflation and interest rate expectations.

Global Developed Equities

Global share markets fell sharply in March as tensions in the Middle East intensified, with the Iran–Israel conflict drawing in the United States and lifting fears of a broader regional escalation.

The jump in oil prices raised concerns about slower growth alongside higher inflation. Historically, large supply-driven oil shocks have often been associated with economic downturns, and this possibility led investors to quickly reduce risk.

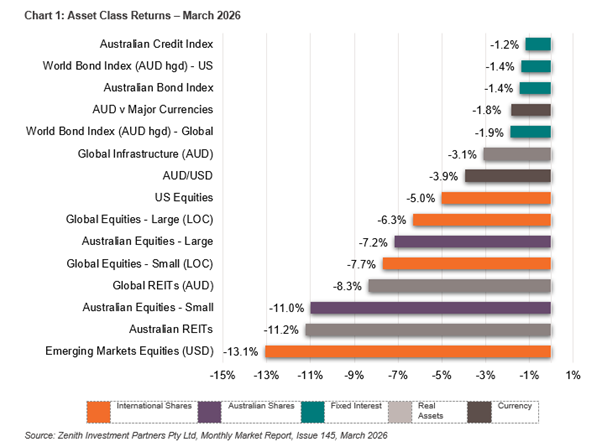

The MSCI World ex Australia index fell just over 6% for the month. Australian dollar returns were slightly better due to currency movements, but gains over the past year were meaningfully reduced as the Australian dollar strengthened earlier in the period.

The sell off was broad, but markets that had strongly outperformed earlier in the year experienced the largest falls. Emerging Asia, Japan and Europe were hit hardest due to their heavy reliance on imported oil and exposure to global growth.

The US market proved more resilient, supported by solid earnings and its position as a net energy exporter. Energy stocks were a clear exception to the broader weakness, delivering strong gains as oil prices surged.

From an investment style perspective, defensive stocks outperformed, while growth and quality stocks lagged. Looking ahead, the market’s direction will depend heavily on whether the Middle East situation de-escalates. A prolonged conflict would remain a clear risk for global equities.

Australian Equities

Australian shares fell more than 7% in March, giving back earlier gains after a relatively strong start to the year. Despite the setback, the market remains well ahead over the past 12 months.

A key driver was the Reserve Bank of Australia’s decision to lift the cash rate again, taking it above 4%. Inflation remains well above the RBA’s target range, and rising oil prices are expected to add further pressure in coming months. With productivity growth weak, the RBA is relying on higher interest rates to slow demand and contain inflation. Markets are currently pricing in the possibility of further rate increases this year.

Company earnings have improved, particularly in the resources sector, helped by stronger commodity prices. Bank earnings have also lifted modestly, though the overall earnings outlook remains relatively restrained.

Sector performance was uneven. Materials shares fell sharply after strong earlier gains, while IT stocks continued to struggle amid concerns about technological disruption. Property trusts were also impacted by higher bond yields.

By contrast, energy stocks performed well, benefiting directly from higher oil prices. Smaller companies underperformed larger firms, reflecting their greater sensitivity to rising interest rates and growth uncertainty.

Emerging Markets

Emerging market equities suffered their worst monthly decline since early 2020, falling more than 13% in March. This followed an extended period of strong performance, driven by improving global growth, a weaker US dollar and optimism around interest rate cuts.

The outlook changed quickly as oil prices spiked and the US dollar strengthened. Many emerging economies are major oil importers, making them particularly vulnerable to higher energy costs. Reduced expectations for global rate cuts further undermined investor confidence.

Markets such as Korea and India were among the hardest hit, reflecting their exposure to both oil prices and global growth trends. China also declined, though it was relatively more resilient due to its strategic energy reserves and greater use of renewable energy.

Despite recent volatility, the medium term outlook for emerging markets remains constructive. Earnings growth expectations are still solid, balance sheets are generally healthier than in the past, and structural growth themes remain intact.

In the near term, however, performance will continue to be closely tied to oil prices, US dollar movements and geopolitical developments.

Property and Infrastructure

Listed property and infrastructure assets reversed earlier gains in March. These sectors had previously benefited from falling bond yields and a rotation away from growth stocks.

However, the surge in oil prices forced markets to reassess interest rate expectations, pushing bond yields higher and reducing the appeal of interest sensitive assets.

Global property and infrastructure markets posted negative returns for the month, while Australian listed property underperformed significantly. Rising real bond yields offset the perceived inflation hedging characteristics of these assets.

Investor sentiment toward the sector remains cautious, particularly while interest rates are rising. That said, infrastructure assets continue to offer longer term appeal due to their essential service nature, though near term performance is likely to remain volatile.

Fixed Interest – Global

Global bond markets fell in March because investors became less confident that interest rates would come down soon. The spike in oil prices increased inflation risk, which led markets to expect fewer rate cuts—and later—across the US, Europe and the UK.

In some cases, investors also started to allow for a higher chance of another rate rise. Short term bond yields rose as investors priced in higher inflation and the risk that rates stay higher for longer.

Longer term yields also rose as real yields increased (in other words, investors demanded a higher return after allowing for inflation). Government bond yields in the US, Europe and the UK moved up to levels not seen for several years.

Credit markets (lending to businesses) also came under pressure. The extra yield investors demand to lend to riskier companies (known as high yield “spreads”) increased, as concerns grew that higher energy costs could slow growth and lift default risks.

Central banks did not need to raise rates again for bonds to fall. Bond prices dropped because markets shifted to a “higher for longer” view—pushing expected rate cuts further out and pricing a higher peak for policy rates.

That lifted yields, particularly on shorter dated bonds, and because bond prices move in the opposite direction to yields, fixed interest returns were negative for the month.

The key issue for bond investors is whether inflation pressures fade quickly or prove more persistent. Continued uncertainty is likely to keep fixed interest markets volatile in the short term.

Fixed Interest – Australia

Australian bond yields rose further in March, reflecting higher inflation, a hawkish RBA and global bond market weakness. The reassessment of interest rate expectations pushed long term government bond yields above 5% for the first time in many years.

The RBA’s latest rate rise was narrowly decided and accompanied by clear warnings that inflation remains a serious concern. While headline inflation eased slightly, underlying inflation is still well above target. At the same time, the labour market remains tight, adding to inflationary pressure.

Markets now expect interest rates to peak higher than previously forecast. This has negatively impacted bond prices but also improved longer term income prospects for investors. Once inflation stabilises, higher yields may provide a more attractive starting point for future bond returns.

Commodities and Currencies

Commodity markets were dominated by oil, with prices jumping more than 60% as the Iran–Israel conflict escalated and the risk of direct US involvement increased, raising concerns about potential supply disruptions and transport chokepoints across the region.

While some easing is expected over time, oil prices are likely to remain elevated while escalation risks persist. Higher oil prices also contributed to broader market volatility.

In currency markets, the US dollar strengthened as investors sought safety and reassessed interest rate expectations.

Other major currencies weakened against the US dollar.

The Australian dollar initially held up due to higher interest rates and commodity exposure but later fell as concerns about global growth turned in the month. Overall, currency movements reflected heightened uncertainty rather than changes in long term fundamentals.

Key Takeaways for Investors

- Geopolitical risks can quickly reverse market sentiment and drive sharp short term volatility.

- Higher oil prices increase inflation risks and reduce the likelihood of near term interest rate cuts.

- Equity market leadership can change rapidly, with defensive and energy assets benefiting in uncertain periods.

- Higher bond yields may pressure prices now but improve longer term return potential.

Bottom Line for Investors

March was a reminder that markets are highly sensitive to unexpected global events, particularly when they affect inflation and interest rates.

While short term volatility has increased, long term fundamentals remain sound in many areas.

Maintaining diversification, staying focused on long term goals and avoiding reactive decisions remain critical when navigating uncertain market conditions.

Looking for Personal Financial Advice?

This investment update is a general overview of market movements for the month. For personal financial advice to achieve your investment goals, contact your FMD adviser.

If you're new to FMD, but ready to get serious about planning your financial future or a worry-free retirement, book an initial discovery meeting with one of our financial advisers in Melbourne, Adelaide or Brisbane.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.