Economic Snapshot: Markets rotate seeking stability

Global markets generally moved higher in February, although leadership shifted away from large US technology stocks.

Investors became more cautious about whether heavy spending on artificial intelligence will translate into sustainable profits, prompting a rotation toward value-oriented sectors, smaller companies, infrastructure and property.

Economic growth remained reasonably solid, but rising geopolitical tensions and concerns about AI-driven job losses pushed government bond yields lower.

Non US markets outperformed the US, with Japan and emerging markets leading gains. Australia also performed well, supported by strength in banks and resources, which are seen as less vulnerable to AI disruption. Government bonds delivered positive returns and outperformed corporate bonds as investors sought stability.

Late in the month, geopolitical risks escalated, particularly in the Middle East. While this occurred after markets closed, it contributed to higher oil prices and increased volatility heading into March.

The Australian dollar continued to strengthen, supported by higher commodity prices and differences in interest rate settings across countries.

Global Developed Equities

Global developed share markets rose modestly in February, with the MSCI World ex Australia Index up 0.6% for the month and 21.2% over the past year. Returns varied significantly by region and sector. US equities lagged, falling 0.9%, as investors reduced exposure to large technology companies despite generally solid earnings results.

Concerns centred on the scale of AI investment and uncertainty over future returns, particularly for software as a service (SasS) businesses, which experienced valuation declines.

Outside the US, performance was stronger. Japanese equities rose 8.6% in February and are now 44% higher over 12 months, supported by improving economic conditions and a decisive election result that provided political stability. European shares gained 2.7%, while UK equities rose 5.1%.

Sector performance reflected the broader rotation in markets. Defensive and value oriented sectors performed well, with materials, utilities, energy and consumer staples rising between 8% and 10%, while information technology declined 3.5%. Falling bond yields and resilient global growth remain supportive, although higher oil prices and lingering inflation pressures continue to pose risks.

Australian Equities

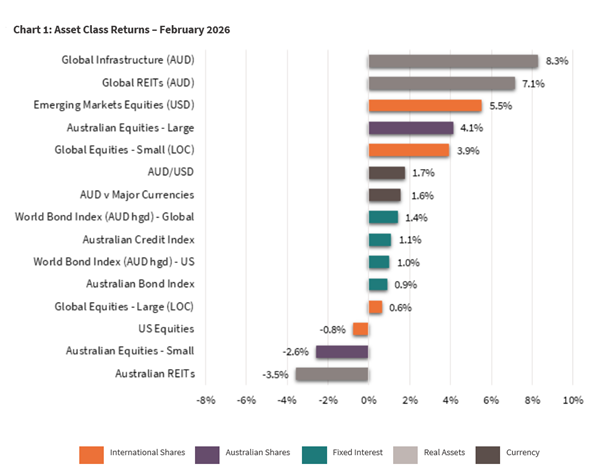

Australian shares continued their strong run, rising 4.1% in February, supported by higher commodity prices and renewed investor interest in banks. Financial stocks led the market, with bank shares up 13.5%, despite already elevated valuations and only modest earnings expectations. Resource stocks also performed strongly, rising 9%, taking their 12 month return to 61%.

Not all sectors benefited. Health care shares fell sharply, down 13.4% in February, leaving the sector 30% lower over the past year. Consumer staples and energy stocks were among the better performers as investors favoured more defensive and inflation resilient exposures.

Economic data surprised on the upside. December quarter GDP grew 0.8%, lifting annual growth to 2.6%. While positive, this strength has reinforced expectations of further interest rate increases. With core inflation at 3.4% in January, markets now expect the cash rate to rise to around 4.3% over the next year.

Mid and small cap shares lagged large caps, reflecting their greater exposure to growth stocks and sensitivity to higher interest rates.

Emerging Markets

Emerging market equities delivered strong returns in February, rising 5.5% in US dollar terms and 30.9% over the past year in Australian dollar terms. Performance was led by Asia and Latin America.

Korea surged 22%, driven by semiconductor and automotive companies, while Taiwan rose 12.8%. Brazil also posted solid gains of 3.9%, supported by attractive valuations and expectations of easier monetary policy.

China was a notable underperformer, falling 5.8%, as concerns about slower long term growth persisted. Authorities reaffirmed a growth target of 4.5–5%, reinforcing expectations that China’s economy is transitioning to a lower growth phase.

Overall, the outlook for emerging markets remains constructive. Earnings growth is expected to be around 20%, supported by higher commodity prices, a weaker US dollar and ongoing demand linked to AI related investment.

Geopolitical risks and sustained high oil prices remain the key downside risks.

Property and Infrastructure

Global listed property and infrastructure performed strongly as investors rotated away from growth stocks. Lower bond yields and a search for stable income supported the sector. Global REITs rose 7.1% in February, lifting their 12 month return to 14.3%, while global infrastructure gained 8.3%, taking annual returns to 21.5%.

Australian listed property lagged global peers, falling 3.5%, largely due to weakness in Goodman Group. Despite this, global infrastructure and property continue to benefit from their defensive characteristics and potential to gain from increased investment in data centres, energy networks and transport assets linked to structural growth themes.

Fixed Interest – Global

Global bond markets delivered positive returns in February as government bond yields fell across major regions. Softer US labour market data, geopolitical uncertainty and anxiety around AI related disruption increased expectations that central banks may cut rates later in the year.

US Treasury yields declined, finishing the month just below 4%. In contrast, corporate bond markets underperformed. Credit spreads widened for both investment grade and high yield bonds, reflecting higher uncertainty and increased issuance by large technology companies funding substantial capital expenditure. US high yield spreads increased from 2.85% to 3.12% during the month.

This means investors now want more extra return for lending to riskier US companies, compared to safer government bonds.

In Europe, bond yields also moved lower. Eurozone inflation eased to 1.7%, its lowest level since 2021, allowing the European Central Bank to hold rates steady at 2%. The Bank of England also left rates unchanged at 3.75%, although markets expect a cut later in March.

Overall, government bonds benefited from their defensive characteristics as investors sought stability amid rising global risks

Fixed Interest – Australia

Australian bond yields edged lower in February, with 10 year yields around 4.65%, still roughly 0.7% higher than US yields. The gap reflects Australia’s more persistent inflation pressures and a stronger domestic economy.

Core inflation remained elevated at 3.4%, signalling that price pressures are proving more entrenched than previously expected.

Stronger household spending, improving business conditions and low unemployment — now at 4.1% — suggest demand is running ahead of the economy’s capacity to supply. As a result, the Reserve Bank of Australia has adopted a more cautious stance, highlighting that the economy may be operating beyond its “speed limit”.

Markets now expect two further interest rate increases, taking the cash rate to around 4.3% over the next 12 months. While falling global yields provided some support, Australian fixed interest remains sensitive to inflation data and domestic economic strength.

Commodities and Currencies

Commodity prices were mixed in February but moved sharply higher toward month end. Gold rose 7.9% during the month and is now up over 80% for the year, reflecting ongoing demand for safe haven assets. Iron ore prices eased to around US$99 a tonne, partly due to softer conditions in China.

Oil prices rose late in the month as tensions escalated in the Middle East. Brent crude finished February near US$72 a barrel before surging above US$100 in early March following disruptions to shipping routes.

The Australian dollar strengthened further, rising 2.2% in February and 14.1% over the past year, supported by higher interest rates relative to the US and firm commodity prices.

Key Takeaways for Investors

- Markets are rotating away from high growth technology stocks toward more traditional and defensive assets.

- Geopolitical risks and inflation remain key drivers of volatility across asset classes.

- Bonds have regained their defensive role as uncertainty has increased.

- Australia has benefited from its exposure to banks and resources but faces ongoing inflation challenges.

Bottom Line for Investors

February highlighted a clear shift in market leadership, with investors favouring resilience and valuation over growth at any price.

While economic conditions remain broadly supportive, elevated geopolitical risks and persistent inflation mean markets are likely to remain volatile.

Maintaining diversification across asset classes and regions remains critical in navigating the period ahead.

Looking for Personal Financial Advice?

This investment update is a general overview of market movements for the month. For personal financial advice to achieve your investment goals, contact your FMD adviser.

If you're new to FMD, but ready to get serious about planning your financial future or a worry-free retirement, book an initial discovery meeting with one of our financial advisers in Melbourne, Adelaide or Brisbane.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.