Economic Snapshot: Markets resilient despite geopolitical risk

January was marked by heightened geopolitical tensions and uncertainty around US policy, yet global share markets proved resilient.

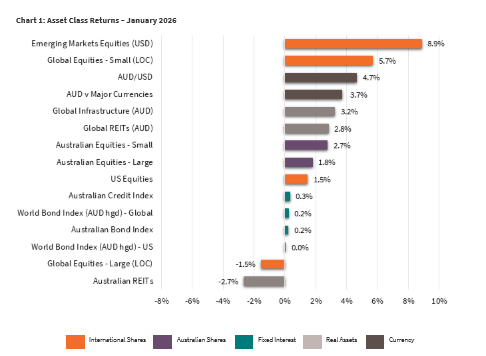

Global equities rose by around 2% in US dollar terms for the month. Australian investors, however, saw weaker returns from overseas shares as the Australian dollar strengthened sharply, reducing unhedged global equity returns.

Bond markets struggled as economic data surprised on the upside, leading investors to reassess expectations for interest rate cuts and pushing yields higher.

Commodity markets stood out, particularly gold, which performed strongly as investors sought protection from geopolitical risks and policy uncertainty.

Importantly, market leadership broadened during the month. Returns were no longer dominated by a small group of large technology stocks, with emerging markets, smaller companies and resource-related sectors outperforming.

Overall, January highlighted the benefits of diversification, as returns varied widely across asset classes, regions and currencies.

Global Developed Equities

Global developed equity markets continued to benefit from a supportive economic backdrop. Economic growth remains resilient across major regions, while inflation has eased from recent peaks.

Corporate earnings expectations have improved, supported by steady consumer demand and ongoing investment. In the US, employment growth has slowed, but unemployment remains low, helping sustain spending and broader economic momentum.

A key theme in January was the broadening of equity performance. Global developed equities rose by around 2% for the month in local currency terms, but gains were no longer concentrated in a handful of large technology companies.

In the US, smaller companies rose by roughly 5%, significantly outperforming large technology stocks, which gained closer to 1%.

Value-oriented and cyclical sectors such as banks, energy and materials performed well, supported by higher commodity prices and confidence that growth is holding up, while the technology sector lagged.

Central banks played an important role in shaping sentiment. The US Federal Reserve held interest rates steady and signalled a more neutral stance, suggesting rates may remain higher for longer rather than falling quickly. Geopolitical developments added volatility but did not derail markets.

Overall, global developed equities remain supported by reasonable growth and improving earnings, although policy uncertainty and geopolitical risks remain key considerations.

Australian Equities

Australian shares started the year positively, supported by rising commodity prices. The ASX 200 rose 1.8% in January, with the materials sector a standout performer, gaining 9.5%.

Over the past year, materials stocks have delivered returns above 40%, significantly outperforming the banking sector.

A major development was the shift in interest rate expectations. The Reserve Bank of Australia raised the cash rate to 3.85% in early February in response to persistent inflation and strong domestic demand.

While the move was described as an adjustment rather than the start of a new tightening cycle, it signals reduced tolerance for inflation remaining above target.

Improving economic conditions are helping the earnings outlook after several years of relatively flat growth.

Resource companies remain central to this improvement, particularly those exposed to copper, which is benefiting from long-term demand linked to electrification and energy transition. Smaller and mid-sized companies, which have higher exposure to resources, also continued to outperform.

Emerging Markets

Emerging markets delivered a strong start to the year, building on their best annual performance in several years.

Emerging market equities rose close to 9% in US dollar terms in January and have returned more than 25% over the past 12 months in Australian dollar terms. Gains were broadbased, with Asia and Latin America leading.

Korea was a standout performer, supported by strong export momentum and strength in technology, particularly semiconductors and advanced manufacturing. Taiwan and China also posted solid gains, while Brazil rose sharply on improving confidence around inflation, interest rates and valuations.

In contrast, India lagged other emerging markets amid concerns about slowing growth and relatively high valuations.

China remains a mixed picture. While exports and newer technologyrelated industries such as robotics and electric vehicles are showing signs of strength, domestic demand and the property sector remain under pressure.

Looking ahead, the outlook for emerging markets is generally constructive, supported by expectations of solid earnings growth, higher commodity prices, a weaker US dollar and ongoing demand linked to technology and energy transition themes.

Property and Infrastructure

Listed property and infrastructure delivered modest gains in January but continued to lag broader share markets over the past year.

Global listed property rose around 3% for the month, while infrastructure gained just over 3%. Australian listed property underperformed, falling during the month and delivering low singledigit returns over the past year.

Performance in these sectors remains closely tied to movements in bond yields and real interest rates.

While inflation has supported rental income and cash flows, higher real yields have weighed on valuations.

Infrastructure assets performed relatively better than property, reflecting their more defensive income characteristics.

These sectors may regain favour if bond yields stabilise, but for now remain more subdued compared with highergrowth areas of the equity market.

Fixed Interest – Global

Global bond markets faced headwinds in January as investors reassessed the outlook for growth, inflation and interest rates.

Stronger economic data reduced expectations for nearterm rate cuts, pushing bond yields higher despite ongoing geopolitical uncertainty. This suggests markets remain more focused on persistent inflation and fiscal pressures than on traditional safehaven demand.

In the US, the Federal Reserve held rates steady at around 3.5–3.75% and shifted to a more neutral stance. Policymakers upgraded their assessment of economic activity to “solid” and noted signs that the labour market has stabilised rather than continued to cool. As a result, the US 10year bond yield rose above 4.2% during the month.

Japan also saw a sharp rise in bond yields, raising the possibility that Japanese investors may reduce their holdings of overseas bonds.

Credit markets remained relatively calm. Investmentgrade and highyield spreads stayed near historically low levels, indicating that investors continue to expect low default rates and ample liquidity.

Overall, global fixed interest markets remain sensitive to incoming economic data and central bank messaging.

Fixed Interest – Australia

Australian bond markets were shaped by a reassessment of inflation risks and domestic monetary policy.

Persistently higher inflation, including core inflation of around 3.4%, alongside strong household spending and improving business investment, prompted the RBA to lift the cash rate to 3.85% in early February, marking the first rate increase in two years.

The RBA has emphasised that the economy is operating above its sustainable speed, reflecting strong demand and weak productivity growth.

While the central bank has avoided committing to a prolonged tightening cycle, it has left the door open to further rate increases if demand does not slow. Market pricing now reflects the possibility of additional tightening later in the year.

Recent economic data supports this cautious stance. Unemployment has fallen to around 4.1%, and business surveys point to improving conditions and rising confidence.

As a result, Australian fixed interest markets are likely to remain volatile, with returns closely linked to inflation outcomes and future policy decisions.

Commodities and Currencies

Commodities started the year strongly, led by gold, which surged on geopolitical risks and central bank buying before pulling back later in the month.

Oil prices also rose sharply due to increased geopolitical risk, while copper continued its strong longer-term upswing, supported by supply constraints and structural demand linked to electrification.

Iron ore prices were relatively stable, constrained by ongoing weakness in China.

Currency markets were dominated by a weaker US dollar, reflecting policy uncertainty and fiscal concerns.

The Australian dollar outperformed, rising above US 70 cents for the first time in several years, supported by higher interest rate expectations and strong base metal prices.

Movements in currencies played a meaningful role in shaping returns for Australian investors with offshore exposures.

Key Takeaways for Investors

- Market returns are broadening beyond a small group of large technology stocks, highlighting the value of diversification.

- Higher interest rates are creating challenges for bonds but supporting returns in commodities and resource-linked equities.

- Currency movements, particularly a stronger Australian dollar, are having a significant impact on offshore investment returns.

- Diversification across regions, sectors and asset classes remains critical in a shifting market environment.

Bottom Line for Investors

Markets are entering 2026 with a blend of opportunity and uncertainty. Earnings remain solid, inflation pressures are easing globally, and interest rate cuts are moving closer -all of which support a constructive outlook.

At the same time, persistent inflation in Australia, questions around AI-driven valuations, and shifting central bank leadership introduce potential volatility.

In this environment, staying diversified across regions, sectors and asset classes remains the most effective way to balance growth opportunities with resilience.

Looking for Personal Financial Advice?

This investment update is a general overview of market movements for the month. For personal financial advice to achieve your investment goals, contact your FMD adviser.

If you're new to FMD, but ready to get serious about planning your financial future or a worry-free retirement, book an initial discovery meeting with one of our financial advisers in Melbourne, Adelaide or Brisbane.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.