Economic Snapshot: Markets react to new risks

Summary

November started well enough for risk assets. US equities rose on some good earnings reports, while UK and European equities gained after the Bank of England and the ECB dialled back expectations of tighter monetary policy. Jerome Powell was reappointed Chairman of the Fed, which the markets liked, and President Biden’s US$550 billion infrastructure package was passed by Congress.

The US economy continues to grow solidly, and the fiscal package adds to the likelihood this could persist for some time. Although good for employment prospects, the additional spending adds to the risk of higher inflation if the COVID-induced supply chain problems are not resolved. US inflation in October remained stubbornly elevated. The Federal Reserve is starting to walk away from talking about “transitory” inflation pressures and has flagged the end of its bond-buying program, with an increasing likelihood this will happen sooner rather than later.

The prospect of firmer than expected US monetary policy, combined with the emergence of the Omicron COVID variant, pushed risk assets down sharply at the end of the month. Equities, commodities, and the A$/US$ all fell.

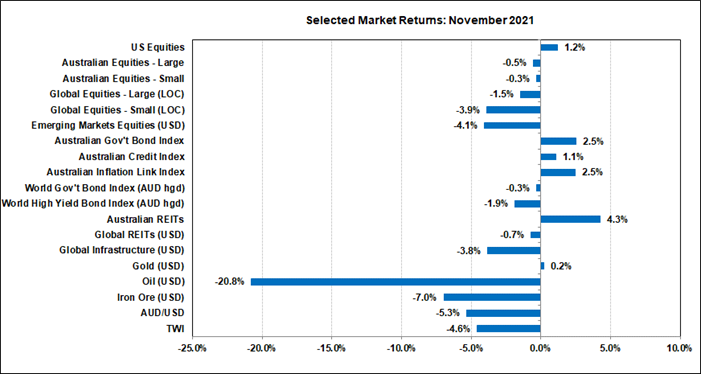

Chart 1: November saw renewed volatility on concerns about US monetary policy and COVID-19

Source: Thomson Reuters, Bloomberg 1 November 2021

Global Financial Markets

November saw financial markets continue to grapple with finding a balance between the good news of recovering economies, the bad news of rising inflation risks, what central banks might do about those risks, and the ever-present threat from COVID. Much of the issues economically were focussed on the US, while the COVID issues are more global. What had been developing as a reasonable month for markets gave way to a renewed bout of volatility towards the end of the month when prices of risk assets dropped sharply.

Overall, the global economy has continued to recover well. For example, measures of growth in the US are at multi-decade highs, business confidence in Australia picked up sharply, French GDP surpassed pre-COVID levels, and consumer confidence is recovering in Japan. To be sure, the picture is uneven both within and across countries. Growth in China is slowing, labour market improvement in several countries has not progressed as far as needed, and there are still supply chain issues around the world.

Labour Markets and Supply Chains

The latter two issues are related because the labour market has been contributing some major distortions to supply chains. The US provides a good example of this. Employment growth in the US in October was solid and the unemployment rate dropped slightly to 4.6%. However, the labour force participation rate – the share of the working age population actively in the labour force as either employees or unemployed – has yet to fully recover from the sharp drop caused by COVID. This means the supply of labour is less than it was before COVID. However, the strong economy has lifted the demand for labour and encouraged workers to move from one job to another in search of higher wages. These conditions are highly conducive to wage inflation and that is what we are seeing in the US where the rate of growth of average hourly earnings is the highest it has been in decades. If spending from the US$550 billion infrastructure package passed by Congress gets to the economy faster than labour supply can pick up, then the risks are that US wage and price inflation will remain higher for longer.

Australia

Conditions here in Australia are not quite the same. The latest labour market figures show the participation rate below its pre-COVID levels, but the lockdowns in Victoria and NSW dampened the demand for labour. Employment fell by 46,300 in October and although the unemployment rate fell, the underemployment rate rose. The wage price index rose 0.6% in the September quarter and 2.2% over the year. This rate of wages growth is still well below the 3% flagged by the Reserve Bank as being necessary for sustained inflation consistent with the Reserve Bank’s objectives. Although the Reserve Bank revised up its growth forecast for the Australian economy and announced the end of its policy to hold three-year bond yields down, it pushed back on market expectations for interest rate hikes to begin in 2023. The Reserve Bank wants to see solid evidence of sustained inflation within its target range before it will act on interest rates.

US Inflation increases

In addition to higher wages, higher oil and food prices have also pushed up inflation in the US. Although central banks are more concerned with inflation excluding energy and food, households still feel the impact at the headline inflation level. The price of oil has risen significantly this year as OPEC restricted supply in the face of the global recovery. However, after peaking around US$84/barrel at the end of October, the price of oil fell 21% to US$66/bl by the end of November. Factors behind this include moves by the US to release oil from its strategic reserves, as well as the emergence of Omicron towards the end of November.

Emergence of Omicron

Many countries including Europe, the US, Canada and parts of Asia and South America, have already seen new waves of COVID delta in recent weeks. The emergence of Omicron in some Southern African countries was a fresh deflationary shock to financial markets. On top of this, towards the end of November Federal Reserve Chairman Powell commented that inflation has been more persistent than expected and that the Fed may have to accelerate its plans to withdraw monetary stimulus.

Market Response

Markets would not have liked either one of these developments, but the two together were especially bad news. Equity markets, which had posted modest gains through November, fell sharply. The US$ rallied, partly on safe-haven demand in the face of Omicron and partly on expectations of tighter Fed policy. The A$ fell from around US$0.75 in early November to around US$0.714 by the end of the month. The A$ is regarded as a more growth-oriented currency than the US$ and so tends to fall in the face of global deflationary shocks like COVID. The A$/US$ rate is now trading well below the levels implied by the bond differentials. This is a good example of markets pricing an increased risk premium into the A$.

Commodities

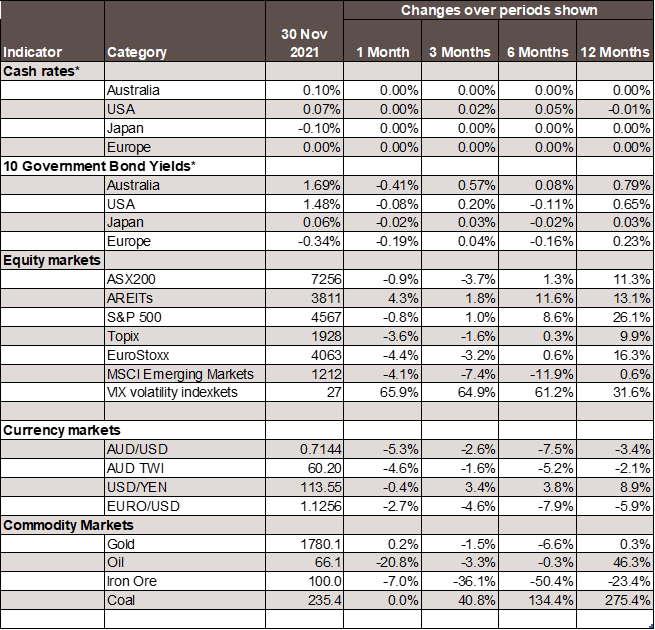

Chart 2: Major Market Indicators – Novemver 2021

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.