Economic Snapshot: Markets continue recovery from December lows - March 2019

The Summary

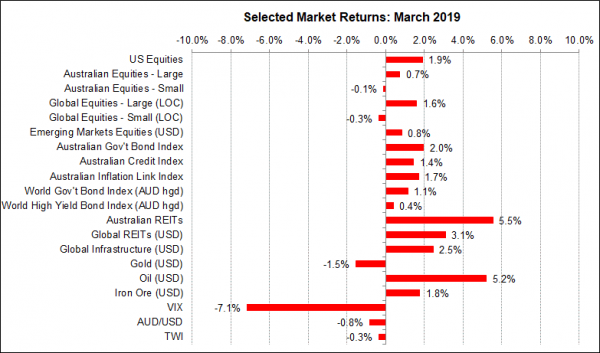

In March, the world’s financial markets continued coming to grips with the implications of the sudden slowdown in global growth in recent months. Data for the manufacturing sector in several major countries confirmed the slowdown and the impact of the US-China trade dispute. However, service sector activity held up well, offsetting some of the concerns. Central banks responded swiftly, shelving planned interest rate increases and re-focussing on liquidity support for banking systems. In both the US and Australia, markets are now expecting interest rate cuts this year and next. This pushed bond yields down even further, with the Australian 10-year government bond yield hitting an all-time low of 1.7%. In turn, this boosted the interest rate sensitive AREIT stocks, which outperformed the rest of the equity market in March. The underperformance of small cap equities compared with large cap equities, both here and overseas, is consistent with concerns about the pace of growth. Expectations of rate cuts also pushed the A$ down, despite higher iron ore and oil prices.

Figure 1: Markets continue their recovery from December lows

Source: Thomson Reuters, Bloomberg 1 April 2019

Australia

Not surprisingly, markets are watching the latest economic data closely to get a handle on the pace of growth. Inflation is less of a concern, as markets believe there will be very little inflationary pressure over the next year or so. Growth and labour markets are what matter most. For example, in Australia the Reserve Bank has made it clear the labour market will be the ultimate driver of what happens to interest rates. Latest data showed further employment growth in February, though not as robust as in the previous month. There was little movement in both the unemployment and underemployment rates, which need to fall further in order to put upward pressure on wages growth.

The Reserve Bank is keen to see higher wage growth because it would help support household consumption, which is such a large part of the economy, and help property owners better manage the impact of declining house prices. However, the Q4 2018 GDP data showed the economy grew by less than expected, with dwelling investment a significant negative contributor. Signs of further house price weakness and falling approvals for new construction suggest we will see more weakness in coming months. The GDP figures also suggested households may be actively reducing their debt levels. Uncertainty ahead of the forthcoming Federal election could be a factor behind this.

Importantly, slowing growth means employment growth slowing in the future. This is a key reason why financial markets now think the Reserve Bank will cut the cash rate twice to 1% by the end of next year, with some analysts predicting the first rate cut as soon as July this year. This sentiment helped push bond yields down further in March. The key 10-year Government bond yield fell to an all-time low of 1.7%. In turn, this helped push up the interest rate sensitive AREIT stocks which strongly outperformed the rest of the equity market in March. Expectations of rate cuts also pushed the A$ down, despite higher iron ore and oil prices.

Global Markets

Elsewhere in the world, the OECD cuts its global growth forecasts, covering all G20 economies. The OECD said the downward revisions were particularly significant for the Euro area, notably Germany and Italy, as well as for the United Kingdom, Canada and Turkey. Consistent with this, there was further evidence of manufacturing activity slowing everywhere. This is partly due to the impact of the trade dispute between the US and China, which has affected not just those countries, but others who trade with them. Interestingly, the data on service sector activity in several major economies was much better than for manufacturing. This confirms the impact of the trade dispute (services are typically non-traded) as well as providing some degree of comfort that the global economy may be able to avoid recession.

The policy response from central banks around the world has been swift. The US Fed, the European ECB, the Bank of Canada, and the authorities in China, were among those announcing steps to support their economies and markets. Planned interest rate increases have been taken off the table and liquidity conditions will be managed to ease pressure on markets and to help the banks in Europe. China also announced tax cuts for businesses and new infrastructure spending. This is particularly important because the sharp contraction in China’s growth late last year is perhaps the main driver of the broader slowdown around the world.

The biggest news came from the US Federal Reserve, which announced an earlier end to Quantitative Tightening. There are likely to be no more rate hikes this year, compared with the two hikes previously pencilled in by the Fed. Rather than being happy with this news, the markets took it as a sign the Fed thinks things are even worse than expected. Bond yields fell as a result and the yield curve briefly inverted (where long-term yields fell below short-term yields). The markets have been obsessed with inverse yield curves in recent months because they believe inversion is an indicator of recession a year or so later. However, history shows inverse yield curves are not a perfect recession signal, and some senior current and past Fed officials commented that there are good reasons why the yield curve post-QE does not mean the same thing as it did pre-GFC.

Geo-political activity

In other developments, Brexit remains a seemingly intractable problem with the UK Parliament unable to find an acceptable plan. Theresa May asked the European Council to extend the Brexit deadline to 30 June, but only got an unconditional extension to April 12. This has since be amended to 31 October. While Theresa May’s days as PM are numbered, it is much less clear when there will be a solution. A “hard Brexit” has seemingly been avoided, for now.

Brexit is not the only geopolitical risk confronting markets. In the USA, Special Counsel Robert Mueller's report said President Trump's campaign did not collude with Russia but left open the question of whether Trump obstructed justice by undermining the investigations in the first place. In addition, Trump has indirectly renewed his attacks on the Fed by nominating an outspoken anti-Fed associate to the Board of Governors. The trade dispute between the US and China continues to be an on-and-off affair with sentiment waxing and waning from one day to the next according to the latest comments from the participants. Markets would welcome a speedy and constructive resolution of the dispute.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Paragem Pty Ltd [AFSL 297276] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Paragem or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.