Economic Snapshot: Australian equities perform well amidst global volatility - February 2019

The Summary

February saw further signs of slowing global growth, muted inflation and ongoing geopolitical risks. Key policymakers have responded with more of the “patience and flexibility” message they have been delivering in recent months. Central banks in Australia, the US, Canada, India, and Europe have all indicated interest rates are on hold for the time being, while EU authorities are showing more willingness to accept a delay in Brexit. Policy pragmatism in the face of global risks is exactly what the markets want to hear. Equity markets had another positive month in February, Australia performing particularly well after a reasonable earnings season and possible interest rate cuts later this year.

Geopolitical events continue to make markets nervous, especially the US-China trade dispute. Latest talks between the US and North Korea ended abruptly as both sides realised they could not reach agreement. The Spanish Prime Minister called a snap election after parliament vetoed the government’s budget. The US government shutdown ended with the President invoking national emergency powers to authorise the building of a wall on the border with Mexico.

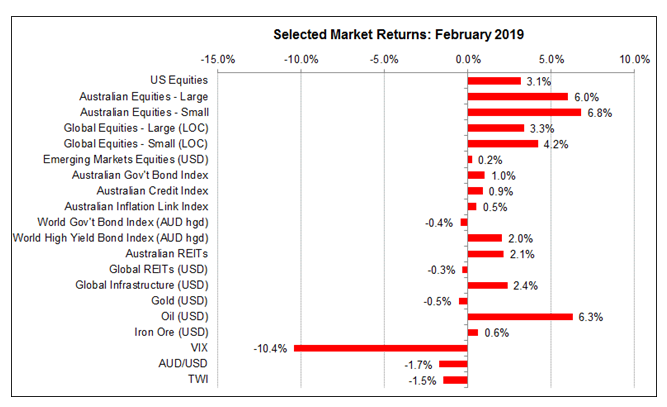

Figure 1: Australian Equities had their best month since mid-2016

Source: Thomson Reuters, Bloomberg 1 March 2019

Australia

The Australian equity market recorded its best result since July 2016, comfortably exceeding global equity market performance. The February reporting season for company profits presented a reasonable, though somewhat mixed, picture with resources companies generally faring better than industrial companies. The local equity market was also helped by commentaries suggesting the economy is slowing enough to warrant the Reserve Bank cutting the cash rate later this year. Much of this debate focuses on the housing sector, where more reports of falling prices are fuelling concerns about adverse wealth effects dampening consumer spending. More tangibly, the data on dwelling permits and starts shows construction activity falling rapidly to levels last seen in late 2012.

Latest figures show domestic business conditions improved slightly in January after falling sharply the previous month. The Reserve Bank downgraded its forecast for economic growth and inflation, as expected, and adopted a more neutral tone about the path of interest rates. In particular, references to the next move in the cash rate being up are disappearing from Reserve Bank commentaries. This contributed to renewed weakness in the A$, which in turn helped the equity market.

USA

Statements from US Federal Reserve officials continued the more moderate tone about interest rates that emerged in December and January. Federal Reserve Chair Jerome Powell reiterated that the Fed would be patient about assessing the need for further interest rate increases depending on how the economic data unfold ed through the year. In addition, two senior Federal Reserve Bank Governors also made important speeches in February. Vice-Chair Clarida and New York Fed President Williams provided valuable insight into how the Fed’s thinking about monetary policy is evolving. Most notably, they outlined circumstances under which the Fed might not lift interest rates even if inflation goes up. This gave the markets further comfort that monetary policy will continue to be more accommodating than previously expected.

Data for the US economy showed the labour market remains in good shape, with another larger-than-expected increase in employment and unemployment at 4%. Manufacturing improved slightly in January after falling sharply the previous month, and wage and price inflation remained subdued. However, estimates for GDP growth in Q1 show the US economy slowed sharply compared with the pace of growth in late 2018. The US government shutdown contributed to this, along with the slower global economy and more specifically the trade dispute with China. These developments are clearly helping reshape the Fed’s thinking about the course of monetary policy over the coming year.

China

Elsewhere in the world, there are continued signs of weaker economic activity. In China the manufacturing sector slowed further, although, it should also be remembered that economic data from China around this time are dampened by the New Year festivities, and usually have some rebound in the following months. Even so, markets are hoping the stimulus provided by the authorities in China will soon start having a positive impact on the economy. Sentiment about the US-China trade dispute waxed and waned throughout the month, but overall the markets seem to expect a broadly favourable conclusion to the current round of talks. It has become more apparent how the trade dispute is hurting both the US and Chinese economies, but there seems to be more pressure on the Chinese authorities to reach a deal, which may happen in the next few weeks.

Europe and the UK

In Europe, official forecasts of growth were downgraded again but, while Brexit continues to be a source of uncertainty for both the UK and Europe, although towards the end of February the markets became increasingly confident that the late March deadline would be extended. This reflected not only developments within the UK, but also comments from the European side, which had been consistently taking a hard line about the terms of exit. The ongoing negotiation for Brexit continues but there is also some feeling that a second referendum may be held with a significantly higher voter turnout.

The deteriorating economic climate makes Europe more vulnerable to downside risks like Brexit, especially at a time when the situation in Italy looks increasingly troublesome. This is likely to have contributed to the Europeans’ more moderate tone towards the UK in recent days.

Finally, the traditional political structure in the UK fragmented further in February with members of both the Conservative and Labour parties leaving to set up a new independent group. This was motivated by the main parties’ attitude towards Brexit, as well as deep dissatisfaction within the Labour Party about Jeremy Corbyn. It is likely we will see more developments like this in coming months with the UK political landscape being gradually reshaped

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Paragem Pty Ltd [AFSL 297276] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at a personal level. No responsibility is accepted by Paragem or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.