Economic Snapshot: Global equity markets rally

The RBA raised the cash rate to 4.1% in June, the highest level since 2012. Surprisingly, they paused rates in July, but another rate hike is expected in August.

Global equity markets rose 3.1% in June, with a 7.6% return for the quarter. The rally included growth stocks, the IT sector, banks, retailers, small caps, REITs, and materials.

The Australian equity market underperformed, rising 1.8% in the month. The underperformance was due to the market’s lower IT exposure.

Global and Australian bond yields increased as markets re-evaluated central bank tightening due to inflation concerns, tight labour markets, and strong growth.

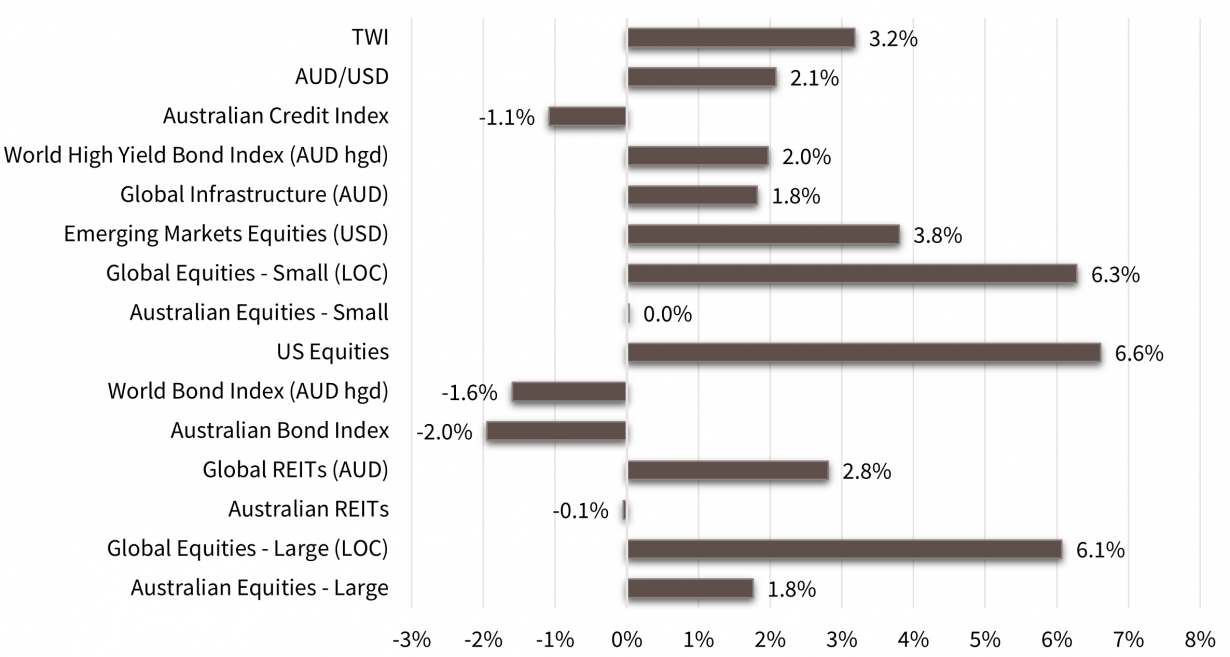

Asset Class Returns - June 2023

Source: Zenith Investment Partners Pty Ltd, Monthly Market Report, Issue 112, June 2023

Global Developed Equities

Global equity markets had a strong rally in June, rising by 6.1% in USD terms, led by growth stocks and the IT sector driven by a focus on AI exposures but broadening to include retailers, small caps, REITs and value stocks.

The MSCI World ex-Australia index was up 18.7% for the year, or 22.6% higher in AUD terms.

Despite expectations of tighter monetary policy and rising bond yields, equity markets have been remarkably resilient.

The focus, more recently, shifted towards positive economic and earnings data, with solid nominal GDP growth, a sound consumer sector, and signs of improvement in the housing market.

Inflation levels varied across regions, but core inflation (price inflation adjusted to exclude more volatile food and fuel components) remains a challenge.

Central banks have so far been willing to risk recession to achieve inflation targets, but economies and labour markets performed better than expected due to overhanging savings buffers from COVID lockdowns and strong jobs and wage growth supported by relatively strong service sectors.

The US market, after lagging European and Japanese markets for much of the rally since October 2022, came to the fore over the June quarter, rising 8.6%, assisted by the large rally in the “magnificent seven” stocks – mega-cap companies, assumed to be the major beneficiaries of the current AI trend, including Apple, Amazon, Alphabet, Meta (Facebook), Microsoft, Nvidia and Tesla.

As mentioned above, the rally broadened out in June with small caps rising 4.2% in AUD terms, taking the June quarter gain to 4.6%.

Japan and Europe ex-UK performed well, driven by factors such as cheap market valuations, accommodative policies, and improved corporate governance.

Australian Equities

Australian equities underperformed global equities, with a 1.8% rise in the month, largely due to a lower IT exposure in the domestic market.

The materials and bank sectors had solid returns in June, but their performance over the quarter was subdued. The health and staple retailing sectors also performed poorly.

The RBA increased the cash rate to 4.1% in early June, the highest level since 2012. RBA governor Philip Lowe expressed concerns about rising costs of labour-intensive services and persistent high services price inflation.

The RBA decided not to raise rates in early July, seen as a pause, with expectations of another rate increase in August.

In June, the materials sector rose 4.7% due to stronger iron ore prices and easing lock-down measures in China.

Banks saw a 3% increase, and insurers benefited from higher bond yields. Insurance and IT were the best-performing sectors for the quarter.

Consumer and business confidence were affected by rising rates, and overall business conditions appeared to deteriorate.

Retail sales rose 0.7% in May, while the overall jobs market remained resilient, with an additional 76,000 jobs created and hours worked increasing too. However, weaker discretionary spending and a softer housing market could impact earnings growth in the period ahead as core inflation remains high, above 6%.

Emerging Markets

Emerging markets had a modest performance, with the MSCI Emerging Markets index up 3.7% for the month (in USD terms) and 5.1% for the year.

Emerging markets have lagged global developed and Australian equity markets in the more recent market recovery.

While countries like Hungary, Poland, Mexico, and Brazil provided returns exceeding 30% for the year, Chinese equities weighed down overall performance.

The MSCI China index experienced a 4% increase in June but declined nearly 10% for the quarter and 16.8% for the year.

Factors such as weak consumer spending, slowing home sales, and a sluggish manufacturing recovery after reopening, contributed to China's poor performance.

Geopolitical tensions and a weaker currency added to the challenges. China's manufacturing Purchasing Manufacturer Index (PMI) remained below 50 for the third consecutive month, and exports declined by 7.5% over the year. Inflation in China remained low compared to other regions.

In response to the challenges, Chinese authorities implemented some stimulus measures in June, including a 10 basis point (0.1%) reduction in the benchmark interest rate.

However, major stimulus prospects remain uncertain due to the deflating property sector and weaker global growth.

India showed strong leading indicators, including PMI readings, while Taiwan and South Korea faced difficulties due to weaker global growth and exports.

Most central banks in emerging markets are maintaining a hold on monetary policy as inflation appears to be peaking.

Property & Infrastructure

A-REITs (Australian Real Estate Investment Trusts) remained mostly unchanged in June but rose 3.4% for the quarter. Despite an 8.1% increase for the year, the sector underperformed equities.

Global REITs saw a 2.8% bounce in the month. For the year, G-REITs were down 5.9%, making it one of the worst-performing sectors.

The focus has been on property valuations, particularly offices due to lower occupancy and higher real yields. Office valuations are being marked down, with some properties being sold at discounts and expectations of a decline in valuations.

Some listed REITs, like Dexus and Charter Hall, have recently announced valuation write-downs, although not as severe as initially anticipated. Meanwhile, sectors such as industrial, health, and data centres have continued to perform well.

Global infrastructure had a 1.8% return in the month but has significantly lagged behind global equities, experiencing a 3% decline for the year.

Fixed Interest – Global & Australia

Global bond yields continued to rise in June as markets reassessed the possibility of central bank tightening due to persistent inflation, tight labour markets, and strong economic growth.

The US 10-year bond yield increased to 3.81%, compared to 3.64% in May and 3.48% in March. Market expectations for the peak Fed funds rate rose to 5.6%, with no anticipation of easing by the end of 2023.

While the US Federal Reserve held off on tightening in June, nine other central banks raised rates, with the Bank of England hiking rates by 50 basis points to 5%.

The European Central Bank (ECB) raised its base rate to 4% and signalled the intention to raise rates further in July.

Australian bond yields saw a significant increase in June, surpassing the 4% level, driven by the upward revisions of the outlook for the RBA cash rate.

The RBA raised the cash rate to 4.1% in early June due to high core inflation, rising wages growth, and a strong labour market. The Bloomberg composite bond index had returns of -1.95% for the month, -2.95% for the quarter, and 1.2% for the year.

The RBA's concern about the rising cost of labour-intensive services and the potential for higher inflation becoming embedded in wages growth led to the rate hike.

However, in a surprise move, the RBA chose not to raise rates further in early July, possibly to observe the impact of previous rate hikes on the economy. Market expectations suggest that rates may reach at least 4.35% in the coming months, with any easing not expected until late 2024.

In other economic news, after the Australian economy added 76,000 jobs in May with the unemployment rate remaining steady at 3.7%.

The NAB business conditions index showed a deceleration in the economy, with confidence remaining subdued.

On a positive note, the strong labour market, higher wages growth, and robust commodity prices resulted in a Federal Budget surplus of $19 billion as of May, providing the government with additional flexibility to fund potential new spending initiatives in future.

Commodities

Commodity prices experienced mixed movements in June, with an overall increase for the month but mostly downward trends for the quarter.

Brent crude oil prices rose by 3% to $74.90 per barrel but were down nearly one-third over the past year. In early June, Saudi Arabia announced a significant cut in output for July, alongside a broader OPEC+ deal to limit supply until 2024, aiming to boost oil prices.

Iron ore prices rebounded in June, reaching $113.50 per tonne after hitting $100 per tonne at the end of May.

While the Chinese industrial recovery has been underwhelming following the reopening of the economy, recent stimulus measures have provided some optimism.

Gold prices drifted lower in June, declining by 2.7% to $1929.40 per ounce, as real yields increased in response to expectations of a higher Fed funds rate for an extended period.

The RBA commodity price index showed a slight increase in June but remained down 21.5% for the financial year.

Currencies

The US dollar weakened in June despite expectations of higher Fed funds rates and the absence of any expected easing in 2023.

The Australian dollar initially strengthened to nearly 69 cents in mid-June, driven by expectations of higher domestic interest rates following a surprise 25 basis point hike and positive jobs and wages data.

However, it weakened towards 66 cents by the end of the month as markets reassessed the outlook for significantly higher Fed funds rates. A rebound in commodity prices, particularly for iron ore, also contributed to the currency's support.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by FMD Group and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the the information contained in this document. Advice is required before any content can be applied at a personal level. No responsibility is accepted by FMD Group or its officers. Past performance is not an indication of future performance.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.