Economic Snapshot: Global equity market correction - October 2018

The Summary

October saw the most significant pull-back in global equity markets since 2015. A wide range of issues contributed to this, including the US/China “trade war”, the Italy/EU budget dispute, slower growth in China and disappointing earnings from some US tech stocks. But the most important cause was higher bond yields in the US on the back of further strong economic data, combined with statements from US Federal Reserve Bank Chair, Jerome Powell, that the US central bank remains on course to keep tightening monetary policy.

Although the Australian equity market recovered some ground towards the end of the month, the ASX200 still posted its worst monthly return since August 2015. As is often the case after falls like this, some investors see opportunities to buy, while others remain cautious, believing the risks have not yet passed. We see further US monetary tightening posing a particular threat to equities for a while.

The local economy remains in reasonable shape, with business conditions improving and the unemployment rate falling to 5%. However, some key measures of spending are slowing; Underemployment remains high and inflation is still just below the Reserve Bank’s target range. In light of this it is not surprising the Reserve Bank has kept the cash rate unchanged at 1.5%. Unlike in the US, there is no pressing need for the Reserve Bank to tighten policy, which implies further weakness in the A$/US$ rate is to be expected.

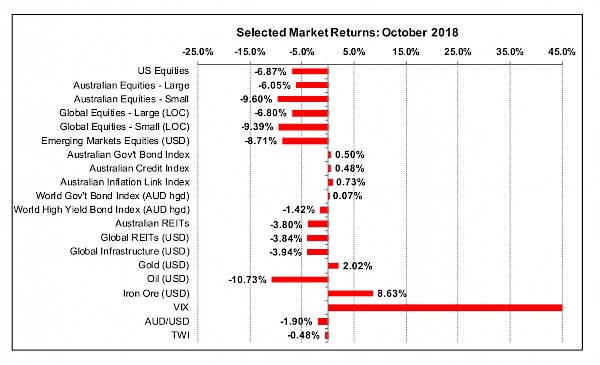

Figure 1: October was a significant correction for equity markets

Source: Thomson Reuters, Bloomberg 1 November 2018

Equity markets around the world experienced a significant correction in October, exacerbated by major indices like the S&P500 falling below key technical levels watched by traders. By 27 October, the ASX 200 Accumulation Index had fallen 8.7% before recovering slightly to finish the month down 6.1%. Small cap stocks, which had been outperforming large caps, underperformed both here and overseas. Australian listed property and infrastructure stocks fared better because they are more interest rate sensitive and the markets thought the sharp falls in equities would make the Federal Reserve soften its stance on monetary policy. This also helped limit the decline in the US exchange rate which lost only 1.9% in the month.

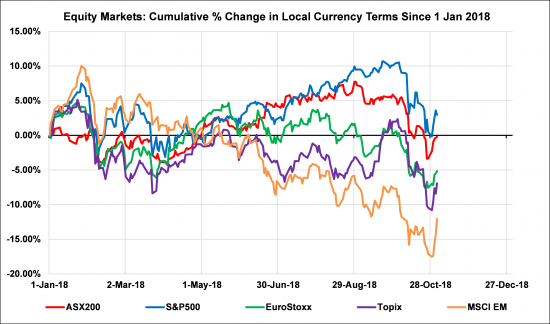

Figure 2 shows cumulative returns in local currency terms since the start of the year for selected equity markets. The losses in October have either wiped out any remaining gains for the year to date or pushed returns even further into negative territory. This highlights that the volatility seen in February this year was not an isolated event, but rather the first stage of a more protracted correction in markets.

Figure 2: Many equity markets have now given up all their 2018 gains

Source: Thomson Reuters, Bloomberg 1 November 2018

Factors driving the volatility

Several factors have been identified as contributing to the October sell-off. These include: The US Fed tightening monetary policy; Disappointing earnings reports from some US tech stocks; The US/China “trade war”; Uncertainty about the US mid-term elections; The budget dispute between Italy and the EU; And in Australia the fall-out from the Royal Commission. Overall, there is plenty for the markets to worry about, but we believe the most important is what the Fed is doing with US monetary policy.

The Fed has made clear it wants to lift the US cash rate from 2.15% now to 3.4% by 2020, while at the same time using quantitative tightening to drain excess liquidity from the economy. Other central banks (but not our Reserve Bank) will be following suit as we move into 2019, but the US will be at the forefront of this tightening of global liquidity. This is because the US economy is running faster than everyone else and must slow down to contain the build-up of prospective inflationary pressures.

However, the markets do not yet believe this narrative. They assume that Fed Chair, Powell, will follow the example of his predecessors and soften the stance of monetary policy when equity markets have sharp falls. All indications are that this is not a good assumption. Powell has inherited an economy in much better shape than his predecessors and has shown no signs of being swayed by market volatility.

The bottom line is that the markets have not yet priced the implications of the Fed’s intentions. As long as this persists, bond and equity markets remain at risk of further weakness.

Rising US bond yields hurt equity market sentiment in October. The key US 10-year government bond yield started the month at 3.08% and quickly rose to 3.25%. Markets saw this as further evidence the multi-decade rally in bond markets is over and were mindful that bond yields around these levels start challenging the valuation of expensive equities. Yields above 3.5% are a particular threat to equity markets, especially now that investors are starting to think US profit growth may have peaked.

In other news:

- The unemployment rate in the US fell to 3.7%, its lowest level since 1969; Other labour market indicators suggest the unemployment rate could fall even further. There has also been a meaningful pickup in growth of wages - all this lends weight to the Fed’s plans;

- There were further signs of weakness in the Australian property sector, with weaker than expected building approvals and more evidence of falling house prices;

- The dispute between the EU and the Italian government over the latter’s proposed budget program continued to put pressure on Italian markets relative to their peers;

- US politics became even more rancorous as the 6 November mid-term elections approached. The Republicans retained control of the Senate, but lost control of the House, leading to policy gridlock. This also contributed to the markets’ nervousness in October;

- There were signs the Chinese economy is still slowing down; The authorities announced further measures to mitigate this.

Finally, US/China trade tensions waxed and waned through the month, with markets taking encouragement from any signs of possible progress. However, this is part of a bigger pushback by the West against China’s economic and military expansion which is now increasingly being seen as too aggressive. The West is seeking to redefine the developing relationship with China, and this too will lead to periodic bouts of market volatility for some time yet.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Paragem Pty Ltd [AFSL 297276] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at a personal level. No responsibility is accepted by Paragem or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.