Economic Snapshot: Financial market respite

Summary

In October, financial markets had something of a respite from the selling of previous months, on hopes that central banks may slow the pace of lifting interest rates. Most equity markets rallied strongly, while bonds had a more modest and somewhat mixed month. The US dollar continued its run of strength, which helped push emerging market equities and the A$ down in September. The price of gold fell through a key technical support level as US real bond yields rose past 1.5%.

On the geopolitical front, the UK wound up with another new Prime Minister with the appointment of Rishi Sunak to replace Liz Truss. Markets are now hoping to see more sense and stability in UK policy making, including not adding pressure on the Bank of England to hike interest rates even further. In China, Xi Jinping has cemented his place as effectively ruler for life, but still faces significant problems bringing COVID under control while trying to stabilise the economy.

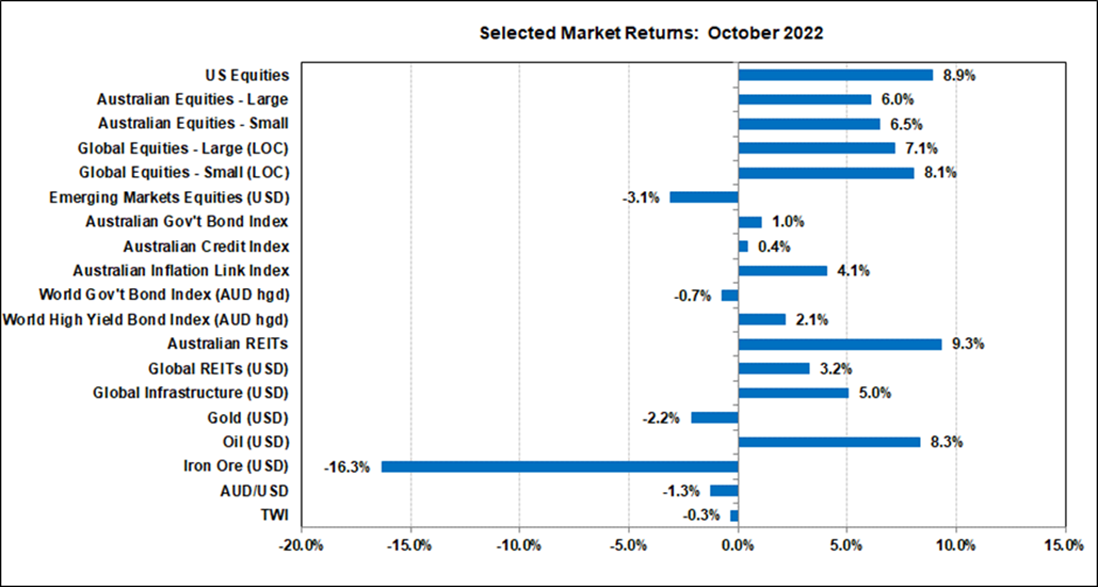

Chart 1: Inflation and higher interest rates undermined markets in September

Source: Equities rallied on hopes of some moderation of rate hikes by central banks

Global Financial Markets

There were a couple of key factors behind the better performance of equities in October. First, markets had sold off heavily through the year and investor sentiment had become very bearish. This provided a favourable environment for a rally when news began to change. Second, investors were hoping the central banks might be far enough through their tightening cycle that some moderation of the pace of interest rate hikes might be imminent.

Interest rates

Some developments which encouraged markets about the outlook for interest rates included comments from the Reserve Bank of Australia and the Bank of Canada that the size of interest rate hikes would likely be reduced to 0.25% a month. The RBA duly delivered a 0.25% increase on 4 October, taking the cash rate to 2.6%.

However, not all central banks followed this lead. The US Federal Reserve delivered another 0.75% rate increase to bring the Fed funds rate to 3.25%. This more aggressive move by the Fed helped push the US dollar higher in October. In Europe, the ECB also lifted the cash rate by 0.75% for the second time, bringing the cash rate to 2%. This followed worse than expected inflation figures in Europe. For example, in Germany inflation was 10.4% over the year to September.

Inflation levels

Inflation in the US in September also exceeded the markets’ expectations. Headline inflation rose 0.4% in the month and 8.2% over the year, compared with 8.3% over the year to August. Core inflation rose 0.6% in September, the same result as for August, and 6.7% over the year, compared with 6.3% over the year to August.

Australian inflation was also stronger than expected in the June quarter. Headline inflation rose 1.8% in the quarter and 7.3% over the year, while core inflation rose 1.8% in the quarter and 6.1% over the year. Housing, energy, transport and food costs were significant contributors to these results. Non-discretionary inflation – that is, goods and services households find harder to cut back on – was well above discretionary inflation. Also, goods inflation is running at about twice as fast as services inflation.

Positive signals

Despite these less than encouraging inflation figures, markets still hoped that signs of liquidity stress in financial markets might induce the Fed to moderate its pace of tightening and add liquidity to the system. For example, the TED spread (US Eurodollar – US domestic 3-month rates) has surged above levels seen in the depths of the Covid crisis. The TED spread is a traditional indicator of US$ liquidity stress, with higher levels of the spread indicating higher levels of stress. Also, the difficulties experienced by Credit Suisse have been interpreted as another sign of liquidity stress. However, it is unclear how much Credit Suisse’s problems are due to liquidity and how much to its own management. So far, the Fed seems aware of, but not responding to, these signals.

The second sign of potential encouragement for markets is data suggesting some slowing of growth which would indicate interest rate increases we’ve seen are starting to bite and that the central banks could be closer to having done all they need to do. This is the “bad news is good news” theme.

In the US there was mixed news about the economy. For example, the key ISM manufacturing index fell to 50.9, however the ISM services index held steady at 56.7. The 50 level on these indices marks the difference between economic expansion (above 50) and contraction (below 50). The labour market is still robust, with another 263,000 jobs added in September and the unemployment rate dropping slightly to 3.5%. Wage inflation eased a little in September.

Australia

In Australia, employment growth stalled in September with only 990 new jobs added, but the unemployment rate remained steady at 3.5%. A key measure of business conditions improved again in September, returning to levels last seen in mid-2021. However, business confidence is more subdued than this, and household confidence is still at its lowest levels since the GFC despite a small improvement in September.

While there are signs of slower economic growth, the picture is uneven between countries, and the central bank response varies not only according to domestic conditions, but also with differences in how each country’s financial system works. Overall, it is too soon to say we are out of the woods as far as rate hikes are concerned. Even though the RBA has slowed the pace of its increases, it has made it clear there are still more to come.

Geopolitical

On the geopolitical front, the UK wound up with another new Prime Minister with the appointment of Rishi Sunak to replace Liz Truss. Markets are now hoping to see more sense and stability in UK policy making, including not adding pressure on the Bank of England to hike interest rates further. In China, Xi Jinping has cemented his place as effectively ruler for life, but still faces significant problems bringing COVID under control while trying to stabilise the economy.

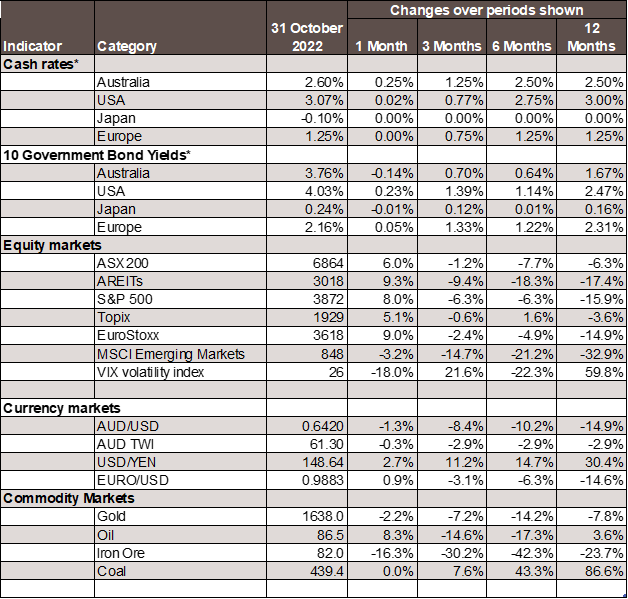

Chart 2: Major Market Indicators – October 2022

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.