Economic Snapshot: Economies reopen for business - May 2020

Summary

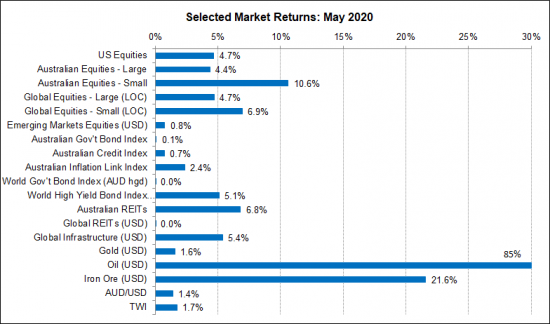

Equity markets pushed higher in May, taking valuations to very expensive levels, as markets took an almost exclusively optimistic view of declining infection rates, reports of progress towards a vaccine and the benefits of economies re-opening. Less promising news on vaccines, still high infection rates in the US, the accelerating spread of the virus in emerging market nations, further weak economic data, and rising geopolitical tensions between the US and China, as well as the rioting in the US, were all dismissed by the markets.

In commodity markets, iron ore had a good month as the supply from Brazil succumbed to the spread of the virus. Similarly, in the oil market, production cuts resulting from OPEC’s recent decisions, as well as in the US from 60% of oil rigs being shut down as lower prices made them unprofitable, helped push the oil price up sharply in May.

The strength of these key commodity prices, along with speculation of a negative US cash rate, pushed the A$/US$ up 1.4% to US$0.666 by the end of the month.

Chart 1: Markets ignored the bad news in May to push higher.

Source: Thomson Reuters, Bloomberg 1 June 2020

COVID-19 Pandemic

There were significant developments in the global Covid-19 situation. Many developed market countries saw progress in reducing the spread of the infection as a result of their lockdowns. The US, UK, Japan, Europe, China and Australia all saw falls in the number of new cases per week compared with a month earlier. However, many emerging market countries saw the opposite and now have accelerating rates of infection. Brazil surpassed the US with the highest number of new infections. Despite this, a number of these countries have started easing restrictions.

Restrictions have also started to unwind in those countries further through the virus experience. This includes countries like Australia, where the virus has been successfully contained, but also Europe where case numbers, although declining, are still significant. The US is of particular concern. Under pressure from Mr Trump and protesters, some states began easing restrictions even as their infection rates continued to climb.

Vaccine

Optimism in the US about a vaccine for the virus probably helped alleviate fears of a second wave of infections following the easing of restrictions, but the news on vaccines was mixed. Moderna announced good results from 8 out of 45 subjects in a Phase 1 trial but said nothing about the other 38 subjects. Within 24 hours doubt was being cast on the robustness of Moderna’s results.

Similarly, high hopes were raised for Gilead’s drug Remdesivir, but by the end of the month reports suggested the treatment was less effective than previously thought.

Geopolitical

Some particularly worrying developments in May included the renewed tensions between the US and China, first over Mr Trump’s attempts to blame China for the virus, and second, over China’s clampdown on Hong Kong. It is now clear the President intends to make China a scapegoat in his election campaign.

Also, the spread of rioting in the US and Mr Trump’s intemperate response, has raised fears of a repeat of the turmoil seen in 1968.

Economic Data

US GDP

The economic data released in May showed just how bad April was, as well as giving some early insights into how May was unfolding. Key data in the US showed real GDP growth fell to -11% in April (year-on-year), which carried on into May.

Unemployment

Unemployment insurance claims rose a further 7.3 million in the first three weeks of May, reaching 40.8 million in total since the start of the crisis. April saw 20.5 million jobs lost, driving the unemployment rate up to 14.7%.

In Australia, nearly 600,000 jobs were lost in April, lifting the unemployment rate to 6.2% and the underemployment rate up to 13.7%. The ANZ-Roy Morgan consumer confidence survey showed confidence had improved from a low of around 65 on late March to 92 in mid-April. Many other countries also reported big increases in unemployment.

Manufacturing & Services

Surveys of activity in both manufacturing and services improved from the very low levels reported in April, but still showed overall growth rates below zero.

Commodities

In commodity markets, iron ore had a good month as the supply from Brazil succumbed to the spread of the virus. Similarly, in the oil market, production cuts resulting from OPEC’s recent decisions, as well as in the US from 60% of oil rigs being shut down as lower prices made them unprofitable, helped push the oil price up sharply in May.

The strength of these key commodity prices, along with speculation of a negative US cash rate, pushed the A$/US$ up 1.4% to US$0.666 by the end of the month.

Equities

Despite the bad news in May, equity markets pushed higher on greater optimism about the virus, as well as news of economies re-opening. Markets are still committed to the V-shaped recovery story. However, equity markets are now looking very expensive. By the end of May, the forward P/E in Australia was now the highest it has ever been, while in the US it was the highest since the Tech bubble.

The UK and European markets also look expensive.

Equity markets rallied in April on hopes the pandemic would be brought under control sooner rather than later, thereby allowing a quicker re-opening of economies. Confidence in stimulus packages around the world encouraged the notion of a “V shaped” recovery and prompted further buying.

Retail investors bought heavily, attracted by the prospect of significantly lower prices. Most of the rally occurred in the first half of the month, with momentum moderating in the second half. Even so, the S&P 500 recorded its best month in over 30 years.

Economic Stimulus response

In this environment, there was renewed speculation about additional policy stimulus. The Democrat-controlled House of Representatives in the US passed a US$3 trillion stimulus package which was immediately rejected by the Republican controlled Senate.

Central banks also pledged further support if necessary. The Reserve Bank left the cash rate at 0.25% but some commentators have suggested that both the Federal Reserve and the RBA should take their cash rates below zero. Both central banks have ruled this out.

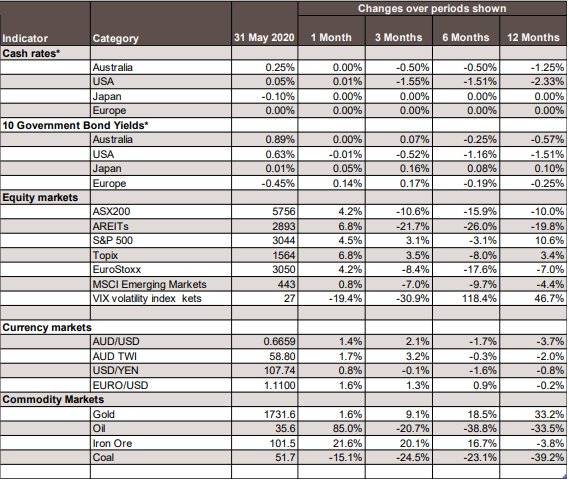

Chart 2: Major Market Indicators - May 2020

*For cash rates and bonds, the changes are % differences; for the rest of the table % changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.