Economic Snapshot: Economic Recovery Strengthens - January 2021

Summary

January saw further improvement in the Australian economy, with higher employment and stronger business conditions and consumer confidence. Inflation rose only modestly in the December quarter to around 1% in annual terms. This is well below the Reserve Bank’s 2%-3% target range.

Economic activity in the US and Europe is showing the impact of new lockdowns to curb the spread of the latest strains of COVID. There are fears of a double-dip recession in Europe. The US election was finally wrapped up with Joe Biden’s inauguration and the Democrats winning the Senate run-off races in Georgia. Biden has proposed a massive spending package but will have to negotiate the details through the Senate. The US bond market greeted this with some concern about whether big spending programs would lead to higher inflation. The yield on 10-year government bonds rose through 1% for the first time since March 2020.

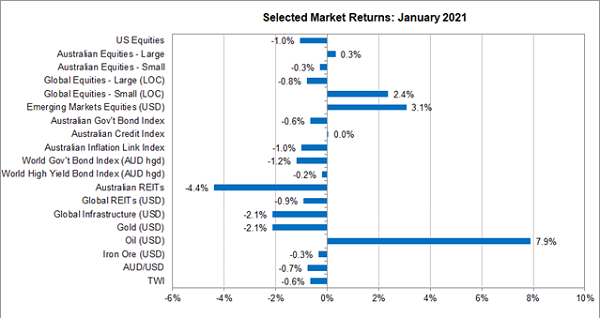

Equity markets, especially emerging equities, were having a good month until pressures from the online trader world spilled over into the broader market by forcing hedge funds to liquidate large short positions. This pushed the US equity markets down sharply in the last week of the month.

The Australian dollar (A$) was surprisingly resilient despite an 8.3% drop in the iron ore price late in the month. The A$/US$ finished at US$0.7645 after reaching US$0.7795 earlier in the month. The price of gold fell 2.6% as it followed the movements in US Treasury Inflation Protected Securities (TIPS) yields.

Chart 1: Pressure from online traders took the gloss off equity markets at the end of January.

Source: Thomson Reuters, Bloomberg 1 February 2021

Continuing impact of COVID-19

COVID continues to be a serious problem around the world. The number of new cases is declining quickly in the US, UK and Japan but remains at elevated levels. Progress in Europe is mixed, with declines in some countries but renewed waves in others. Overall, Europe is holding the line at around 600,000 new cases per week. Compared with these countries, Australia has the virus well under control.

Not surprisingly, the spread of COVID in the Northern hemisphere has been having an impact on economic activity. In the US, employment fell in December although the unemployment rate was steady at 6.7%. The impact was felt most in services industries. The ISM manufacturing index rose again in December to its highest level since February 2018. In Europe, there are fears of a double-dip recession under the impact of lockdowns. Central banks in both the US and Europe reiterated their intentions to maintain highly accommodative monetary policies for some time to come.

Australia

Latest economic data for Australia showed core inflation rose 0.4% in the December quarter and 1.2% over the year to the quarter. Headline inflation rose 0.9% in the quarter and 0.9% over the year to the quarter. Biggest contributors to the quarter’s result were higher prices for alcohol, tobacco, furnishings and household equipment. Both core and headline inflation remain well below the Reserve Bank’s 2%-3% target range.

The NAB Business Survey showed further improvement in business conditions in December, although business confidence slipped back in the month. Consumer confidence remains at its highest levels since 2010. The labour market continued to improve in December, with another 50,000 new jobs and the unemployment rate falling to 6.6% from 6.8% in November.

United States

The US elections were finally wrapped up with Joe Biden’s inauguration and the Democrats winning the Senate run-off races in Georgia. The Democrats and Republicans now have 50 seats each in the Senate, with the Vice-President having the casting vote. However, the somewhat arcane voting rules in the Senate do not make things as easy for the Democrats as the number of seats might suggest. Biden has proposed a massive spending package but will have to negotiate the details through the Senate.

US Bond Market

The US bond market greeted the US Senate results with some concern about whether big spending programs would lead to higher inflation. The yield on 10-year government bonds rose through 1% for the first time since March 2020. At the same time, the yield on inflation protected bonds (TIPS) fell to -1%. This implies the US bond market is now expecting inflation of a little over 2%.

The bond market was also concerned that increased fiscal stimulus would lead to less bond-buying by the Federal Reserve. However, the Fed reassured the markets it will be providing support for some time yet. The Australian bond market followed the US, with our 10-year yield also moving just over 1%. This would have contributed to the underperformance of AREIT’s in January because these stocks are more sensitive to movements in bond yields. The resources sector also had a tough month, falling 8.3% in the last week of January in response to a similar sized fall in the iron ore price.

Equity Markets

Equity markets, especially emerging equity markets, were having a good month until the last week when pressures from the online trader world spilled over into the broader market. Online traders were connecting via Reddit to identify stocks in which hedge funds were running large short positions. The traders then placed massive buy orders on those stocks, forcing the hedge funds to sell other stocks they owned in order to meet their margin calls. The net effect was that the US equity market fell 2.6% on 27 January and a further 1.9% on the 29th, while the stock bought by the online traders rose dramatically.

One result of all this was that the very popular trading platform Robinhood had to impose limits on trades to support the proper processing of unsettled orders. Robinhood suddenly found itself short of the necessary liquidity and had to quickly raise more than a billion dollars to support its operations. Although this may look like a quirky story from a niche part of the market, we are likely to see more of it. Because the trading activity can flow through the brokers back to the clearing houses there are potential systemic stability issues involved. This will be something to watch.

Exchange Rates, Gold Price & Oil

The A$ was surprisingly resilient to the drop in the iron ore price. The A$/US$ fell only about 1% in the last week of the month to finish at US$0.7645 after reaching US$0.7795 earlier in the month.

The price of gold fell 2.6% as it followed the movements in US TIPS yields. The price of oil rose in early January on expectations of higher demand as economies recover, but the rally moderated later in the month as reports of increased supply emerged.

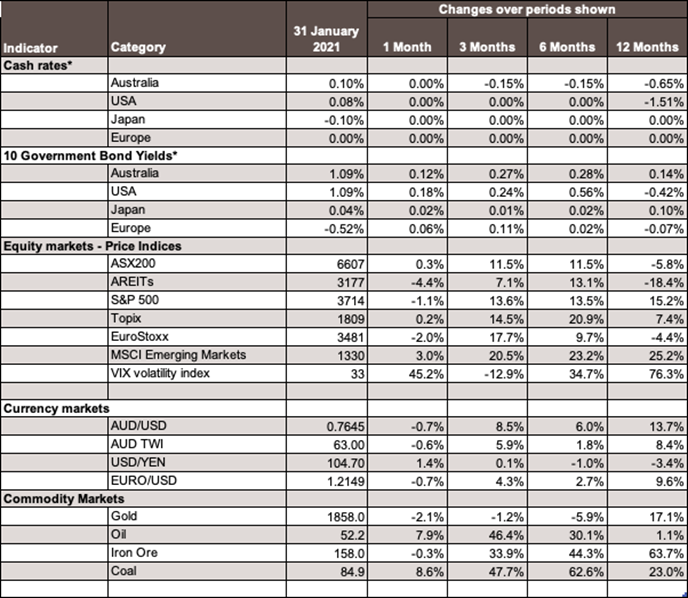

Chart 2: Major Market Indicators – January 2021

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.