Economic Snapshot: Consolidation in global markets

Summary

May was something of a consolidation month for most asset classes. Global investors have been grappling with the trade-off between the benefits of stronger global growth for corporate profits and the potential impact to bond yields and values from higher inflation that might flow from the stronger growth.

In May, the balance of sentiment appeared to shift from inflation to growth, leading bond markets to stabilise and equities to post modest gains despite a number of markets being at record highs.

The A$/US$ traded in line with the interest rate differences between the Australian and US bond yields which slipped over the month despite the higher iron ore price. In recent months the A$/US$ has been dominated by bond yield differentials and has paid less attention to the stronger iron ore price.

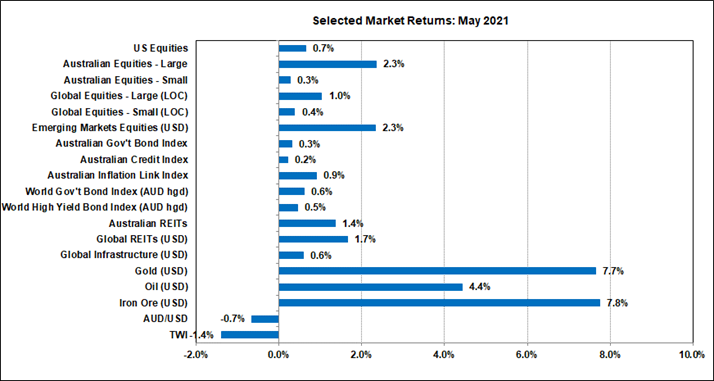

Gold had its best month in a while, driven by the stabilisation of US bond yields and a lower US$.Some commentators have suggested the recent weakness of Bitcoin helped push speculators into gold. Bitcoin fell 35% in May.

Chart 1: May was a consolidation month for most asset classes, but gold did well

Source: Thomson Reuters, Bloomberg 1 June 2021

Global Markets

May was something of a consolidation month for most asset classes. Bonds and equities posted positive returns across the board, but the A$ slipped even though the iron ore price had another strong month.

Global investors have been grappling with the trade-off between the benefits of stronger global growth for corporate profits and the potential impact to bonds from higher inflation that might flow from the stronger growth.

In May, the balance of sentiment appeared to shift from inflation to growth, leading bond markets to stabilise and equities to post modest gains despite a number of markets being at record highs.

Inflation

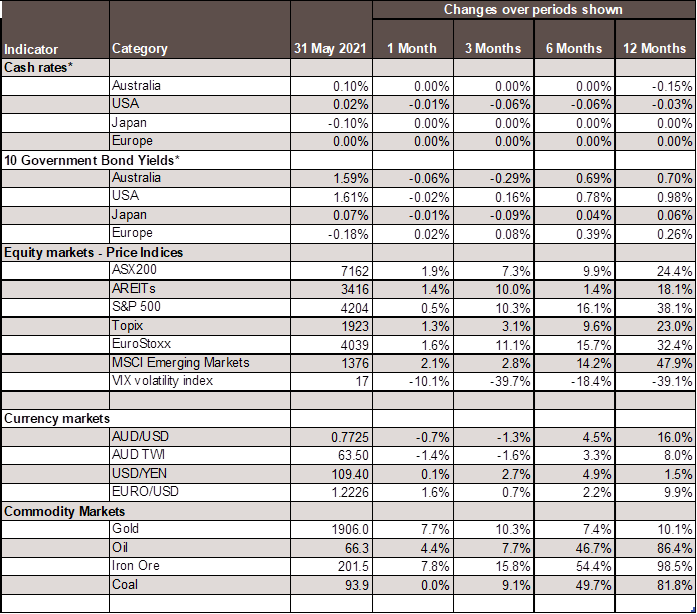

The latest inflation data from the US was higher than expected. Headline inflation in the year to April was 4.2%, while core inflation was 3%.

Economic activity slowed with both the leading ISM (Institute of Supply Management) manufacturing and services indices moderating in May, though still maintaining very respectable levels.

Employment rose strongly in April, but the unemployment rate remained just over 6% as new job seekers entered the labour market.

Overall, while investors are largely focused on the inflation headlines, they have not yet seen enough in the data to be convinced that higher inflation will persist for a long period.

Investors have also been reassured by the Federal Reserve’s repeated message that any immediate signs of inflation are likely to be temporary and not derail the Fed’s accommodative monetary stance.

As a result, US nominal 10-year bond yields finished at the end of May around the same level as at the start of the month, while 10-year inflation-adjusted yields fell slightly.

Financial Markets

The bond market’s pricing of expected inflation had risen in the first half of the month but then eased back again in the second half.

This allowed the US equity market, which lost ground in the first half of the month, to recover that in the second half and finish a touch higher for the month as a whole.

Non-US equity markets performed even better, with European equities helped by prospects for improving growth and progress on managing COVID. Emerging market equities were boosted by a weaker US$.

Australia

Here in Australia, the first quarter inflation (CPI) report came in lower than markets had expected, with both headline and core inflation coming in well below the Reserve Bank’s 2% - 3% target range.

The April labour market report was also softer than expected with a loss of 31,000 jobs, but a small fall in the unemployment rate to 5.5%. Wages growth remains muted with the wage price index rising only 1.5% in the year to the March quarter.

However, measures of business confidence and conditions posted solid gains in April to record highs. Measures of employment within the NAB’s business survey indicate further declines in the unemployment rate in coming months.

The Reserve Bank upgraded its economic outlook, and the Federal Government delivered a pro-growth budget. These factors, plus further strength in commodity prices, helped the ASX200 post a respectable 2.3% gain for the month. Listed property (Australian Real Estate Investment Trusts or AREIT’s) also had a good month, helped by the stabilisation of bond yields that can impact how properties are valued.

Exchange Rates

The A$/US$ traded in line with the Australia/US bond differentials, slipping over the month despite the higher iron ore price. In recent months the A$/US$ has been dominated by the bond differentials and has paid less attention to iron ore.

Gold Price (and Bitcoin)

Gold had its best month in a while. The gold price peaked just over US$2,000/oz in August last year and then declined, with some volatility, to just under US$1,700/oz in March this year. Since then the gold price has bounced back to around US$1,900/oz, most of which happened in May.

The main driver of this rally has been the stabilisation of US bond yields as markets have moved past their initial fears of higher US inflation and tighter monetary policy. Associated with this, the US$ has slipped back as well. These conditions favour a higher gold price.

However, some commentators have noted an apparent inverse relationship between the gold price and Bitcoin. The story goes that gold and Bitcoin are similar speculative assets in that they both have finite supply, but potentially infinite demand. Their prices could theoretically be anything, or nothing.

Some also see them as alternative forms of money to those issued by governments. However, gold and Bitcoin are seen as substitutable, not complementary, assets. That is, speculators sell one to buy the other, but do not buy or sell both at the same time.

Under the influence of social media gossip, the price of Bitcoin fell 35% in May, apparently helping the gold price rise.

Chart 2: Major Market Indicators – May 2021

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.