Economic Snapshot: Central banks cut rates to support growth - July 2019

The Summary

July was all about central banks cutting interest rates to support growth. This spurred equity markets to new highs in both Australia and the US. The Reserve Bank and the Federal Reserve both cut (0.25% in Australia in both June and July and 0.25% in the US). Here in Australia, the cash rate and bond yields are at new record lows.

The RBA said it will now pause to assess the impact of its actions, but did not rule out more cuts, and said the cash rate will likely stay low for a long time. These moves, combined with the passage of the Government’s tax cuts, should provide some support for the economy as we move into 2020. However, inflation is still too low and the unemployment rate too high for the RBA to declare success. The US Federal Reserve disappointed markets by not cutting as much as had been hoped, and by Chair Powell’s clumsy press conference.

This, plus new US tariffs on Chinese goods, pulled equity markets down at the end of the month, but not before both the ASX200 and the S&P500 had reached new record highs. The European Central Bank also said it is ready to cut interest rates and provide more quantitative easing if needed. In the UK, Boris Jonson became Prime Minister and promised to deliver Brexit one way or another by 31 October. The UK political and economic outlook is becoming ever riskier and it is little surprise the markets are punishing the Sterling.

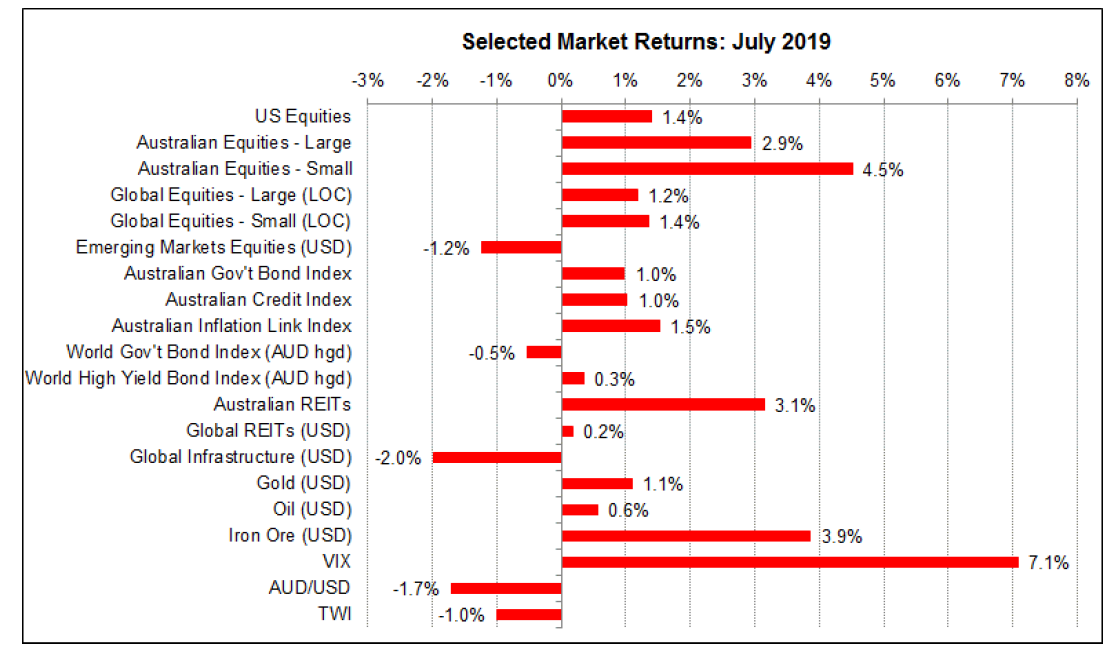

Figure 1: Central bank stimulushelped push equities up in July

Source: Thomson Reuters, Bloomberg 1 August 2019

Australia

The latest economic data in Australia provided a backdrop for the Reserve Bank to cut the cash rate to 1.00%. This was the first time since 2012 that the RBA had cut the cash rate in two consecutive months. The RBA’s focus is very much on spare capacity in the labour market, where employment growth flat-lined in June and the unemployment rate was steady at 5.2%.

Leading indicators still suggest little improvement in unemployment in coming months. On top of this, latest figures on growth of building approvals and retail sales were both weak and measures of consumer and business confidence both fell. June quarter inflation remained subdued, with headline CPI inflation of 1.4%. These results are still well below the bottom of the RBA’s 2%-3% inflation target.

Given these conditions, it is not surprising the RBA cut the cash rate to a new record low of 1.0% in July. Although the RBA wants to assess the impact of its two rate cuts, it did not rule out further cuts if necessary. Governor Lowe said the cash rate will be low for a long time to come, but that it is unlikely the RBA will need to resort to quantitative easing.

The markets still expect more rate cuts in coming months, potentially taking the cash rate as low as 0.50% by early 2020. The RBA’s actions, combined with associated softness of the Australian dollar, and Parliament’s passing of the Government’s tax cut package, are all positive factors for the economy as we move into 2020. Households in particular stand to benefit from these moves. However, while these measures help reduce the odds of imminent recession, more fiscal stimulus and productivity growth is needed.

Markets have been surprised by how quickly the interest rate landscape in Australia has changed in the last few months. However, investors have reacted positively to the RBA’s moves, with bond yields falling to new lows and equities reaching new highs. The ASX200 finally surpassed its November 2007 high of 6829 to reach 6845 on 30 July 2019. The chase for yield in the low cash rate environment has been a powerful driver of investor behaviour.

USA

In the US, the economy is still in pretty good shape, especially the labour market. However, wage growth looks to have peaked and inflation is still below the Fed’s target. Markets had been expecting the Federal Reserve to cut the cash rate by as much as half a percent in July and to then follow up with more cuts in coming months. This, plus reasonable early results in the US earnings season, provided good support for the US equity market. The S&P500 closed above 3000 for the first time on 12 July before slipping back to 2980 by the end of the month.

There were two key reasons for the pull-back. First, the Fed disappointed the markets by delivering only a 0.25% cut and then Chair Powell exacerbated the situation by saying this was an “insurance cut” and not the start of a sustained easing cycle. He then added that this did not rule out more rate cuts. Markets found all this both confusing and disappointing. President Trump used it as an excuse to launch another broadside at Powell.

The second reason was that hopes for an improvement in US-China trade relations took a hit near the end of the month when President Trump announced further tariff increases on Chinese goods. In reality, the markets had probably been getting too optimistic about both trade and interest rates.

Europe and the Unilted Kingdom

In other news around the world, the European Central Bank said it is ready to cut rates and provide more quantitative easing if inflation did not pick up. Mario Draghi, the head of the ECB, is retiring and will be succeeded by Christine Lagarde, the outgoing Managing Director of the International Monetary Fund. Draghi has been one of the best central bankers in the world post-GFC and leaves big shoes to fill.

Boris Johnson became Prime Minister in the United Kingdom and faces the task of making Brexit a reality. However, all the underlying problems are still there and appear as difficult to solve as ever. The Government’s wafer-thin majority in Parliament is very vulnerable and an election before a Brexit deal is quite possible. The polls show the Conservatives and Labour are quite close, despite Corbyn’s radical hard-left agenda. A no-deal Brexit would be a major shock to the UK economy. If this were somehow combined with a Corbyn government, things could get dire indeed. Little wonder the markets are starting to punish the Sterling.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.