Economic Snapshot: A most dramatic half year - June 2020

Summary

2019/20 was the most dramatic year for financial markets since the GFC. The first half of the year was dominated by concerns of global recession as trade tensions and slower growth in China spilled over into the rest of the world. Central banks cut cash rates even further, which encouraged equity markets to rally into December.

The ongoing popularity of tech stocks helped underpin the rally. However, equity market valuations closed 2019 in expensive territory.

The emergence of Covid-19 in the New Year turned everything on its head. Unprecedented conditions around the world, including lockdowns, crushed economic activity and drove equity markets down sharply.

Massive central bank stimulus almost immediately saw cash rates fall to new record lows and vast amounts of liquidity poured into financial markets. On top of this, governments announced trillions of dollars of stimulus. Combined with the central bank moves this sparked an equity rally that ran through to the end of June, once again pushing equity valuations into expensive territory.

As 2019/20 closed, Covid-19 was making a comeback in the US which had never made sufficient progress in containing the virus. Other countries, including Australia, were also experiencing renewed outbreaks, albeit on a much smaller scale. This virus uncertainty remains the major risk facing equity markets, which are vulnerable to bouts of volatility.

Tensions with China, and the US Presidential election are also sources of risk in the period ahead.

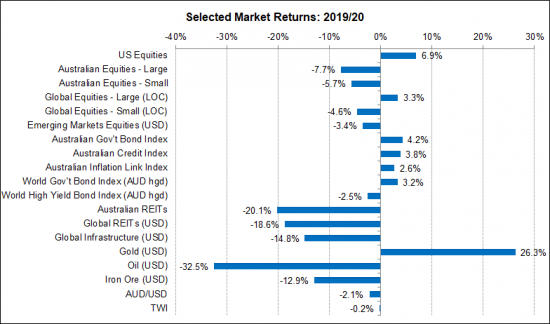

Chart 1: 2019/20 was the most dramatic year since the GFC

Source: Thomson Reuters, Bloomberg 1 July 2020

Key developments in 2019/20

Twelve months ago, the idea of a once-in-a-century global pandemic was not on the radar for anyone, let alone global investors. However, there were plenty of other things for them to worry about; top of the list was the possibility of a global recession.

Inflation was stuck below central banks’ targets and monetary policy was seen as being too tight, despite interest rates already being very low by historic standards. On the geopolitical front, the US/China trade dispute, unrest in Hong Kong, Brexit, and regional tensions involving Iran all added to a general air of uncertainty and concern.

Late 2019: Concerns about Recession

The global manufacturing sector was the focus of worries about global recession. As China’s economy slowed so too did their demand for goods from the rest of the world. Europe felt the impact of this quite hard because countries like Germany, Italy and France have big export markets in China.

Australia was also exposed through demand for iron ore and coal. Unemployment in Australia started to creep up, though in the US the unemployment rate remained at historically low levels around 3.5%.

Central banks stepped up and started cutting interest rates. Here in Australia, the cash rate fell from 1.25% in June 2019 to 0.5% by the end of the calendar year. At the time there was quite a bit of speculation about the need for quantitative easing, but the Reserve Bank said this was highly unlikely and certainly not before the cash rate reached its stated lower bound of 0.25%. The US Federal Reserve also cut the cash rate from 2.5% in June to 1.75% by the end of 2019. In Europe, the ECB pushed interest rates further into negative territory.

As 2019 closed, equity markets took on a more positive tone in response to the interest rate cuts, signs of stabilisation in global manufacturing and news of the Phase 1 trade deal between the US and China.

The ongoing popularity of tech stocks helped push the US equity market up 10% in the second half of 2019, but the local equity market managed only a 3% gain.

Early 2020: Bushfires and initial stages of Pandemic

2020 began on a sombre note, with increased tensions between the US and Iran and the terrible bushfires here in Australia. First reports of a new coronavirus in Wuhan garnered little attention with initial concerns mainly focussed on the impact on China’s economy and how that might flow through to the rest of the world through Chinese demand for global goods. Investment markets were not yet thinking about a global pandemic and the first three weeks of February saw further good performance by global equity markets.

The news from China about Covid-19 seemed to be getting better and the latest economic data was still reasonably positive. However, all this changed very quickly from 21 February when markets suddenly became alarmed by reports of the virus spreading to a number of countries around the world, including Italy, Iran, South Korea and the US. The prospect of major economies being shut down to contain the virus, which we now know will have the worst impact on the global economy since the Depression, confronted markets and policy makers alike.

Market response to COVID-19

March was then the most turbulent month for global financial markets since the onset of the GFC.

Evidence of COVID-19 spreading into Europe triggered a sharp fall in equities and other risk assets, combined with a liquidity squeeze as demand for US$ cash (deemed one of the safest assets to own when uncertainty prevails) rocketed.

Volatility rose across many asset classes, with equities moving up and down by 10% a day. The A$/US$ fell nearly US$0.10 to around US$0.56 as it was sold to provide US$ in exchange. These conditions continued until around the middle of March when central banks stepped in to cut interest rates sharply and implemented programs to supply trillions of dollars of liquidity to global markets and banking systems.

Here in Australia, the RBA cut the cash rate to 0.25% and commenced a major bond-buying program.

These moves by central banks, combined with massive government stimulus programs amounting to trillions of dollars globally, rapidly turned market sentiment around.

Markets then embraced a risk-on mood with a strong rally in equities through the June quarter. No matter how terrible news about growth and employment was, it wasn’t enough to deter the rally as investors were told to “look through” the downturn which would only be a “V shaped” decline in growth, that central banks would always be there to save the day, and that a vaccine would be available soon enough.

While many institutional investors remained sceptical about this optimistic outlook, a legion of retail investors around the world bought equities though online accounts, often with cheap borrowed money.

As the June quarter unfolded and many countries made progress on containing the virus, lockdowns began to be relaxed, in some cases, sooner than had been expected and signs of recovery in consumer spending and hiring began.

Here in Australia, the Government’s programs to support the labour market contributed to this.

Further statements of support from central banks and talk of more government stimulus in some countries also helped market sentiment. Tech stocks did well, especially healthcare and services such as online shopping and entertainment. The ongoing tech rally helped push indices higher but masked some less successful performance elsewhere. For example, Afterpay performed very well, but by 30 June the AREITs index was still 20% lower than a year earlier as commercial and retail properties grapple with the impact of lockdowns.

The close of 2019/20 Financial Year

At the close of 2019/20, cash rates and bond yields were at record lows, and equity prices were doing their best to return to their pre-COVID highs. But equity markets were expensive at those levels at the start of the year and are even more expensive now, at a time when the outlook for earnings is more uncertain than ever.

Looking ahead

Importantly, the cause of the problem remains. Covid-19 is an especially virulent coronavirus which can be contained but is unlikely to be eradicated. Until an effective vaccine is available around the world, there will be limits on global economic activity compared with where we were at the end of 2019.

International travel and migration are the most obvious direct impacts. What is probably the biggest global research program of its kind ever seen is underway as scientists around the world search for a vaccine. History shows there has never been a successful vaccine for a coronavirus, but let’s hope this time is different.

Early success with containing the virus, combined with understandable keenness to ease restrictions, may have engendered a complacency about the virus which is now reminding us it is still there. This has been more apparent in the US than elsewhere. The authorities there were too slow to contain the virus in the first place and started relaxing restrictions too soon, driven by excessive confidence in a vaccine, a misguided sense of individual liberties, and mismanagement by the President.

The result is that the US never got its first wave under control and is now seeing a massive resurgence of infections. So far in July, the number of new infections per week is close to 300,000 which is nearly 50% higher than the previous peak in mid-April. It is hard to believe this will not adversely impact economic activity in coming months.

A number of other countries, including China, Japan, Korea and here in Australia have also seen renewed outbreaks. The bottom line is that in the absence of a vaccine, we need to establish a balance between containment and economic stability. The world has yet to find that balance because we have not been living with the virus for long enough.

Geopolitical environment

On top of this, the geopolitical situation is far from settled:

- Covid-19 has exacerbated existing tensions between a number of countries and China, with more nations openly questioning China’s motives and methods, including recent events in Hong Kong. Although the US is the most vocal in this regard, they are not alone;

- The dramatic ructions in the oil market this year led to a major contraction in global supply, which will impact the revenues of oil-dependent nations such as Russia and Iran and do nothing to ease tensions in the Middle East;

- The US is facing a Presidential election in November, after what is likely to be the most rancorous election season in decades. Polling suggests Mr Trump will lose to Mr Biden, but a lot can happen yet. In general, markets are more comfortable with Mr Trump – despite all his manifest flaws – than with a Democrat administration likely to pursue more anti-business policies.

Global Markets: Where to from here?

So, where does all this leave the markets as we move into the new financial year? Despite the early improvement in some spending indicators, labour markets are still in bad shape.

Unemployment has spiked sharply, and there are fears it will rise further when government support programs end in coming months. Cash rates are at record lows and will stay at these levels for years to come. Inflation is weak and will not return to central bank target ranges for a long time. Equity markets are vulnerable to renewed bouts of volatility. Central bank balance sheets and government debt levels will remain elevated for years to come.

In short, it appears that the “lower for longer” environment investors had been grappling with prior to Covid-19 has been reinforced and extended.

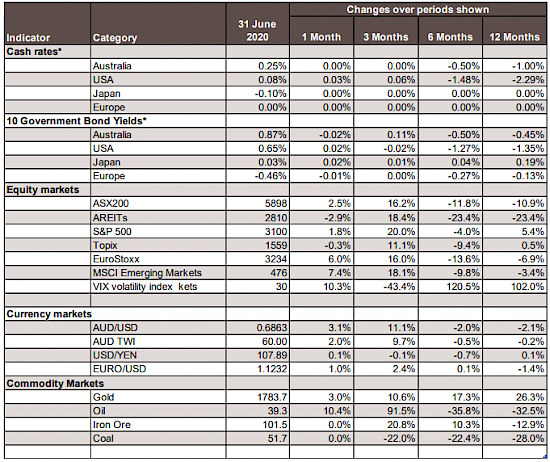

Chart 2: Major Market Indicators - June 2020

*For cash rates and bonds, the changes are % differences; for the rest of the table % changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.