Economic Snapshot: The legacy of the GFC - August 2018

The Summary

It’s been a decade since the peak of the Global Financial Crisis and the legacy remains clear. While equity markets have had some outstanding returns since that time – with a range of markets at record levels – policy-makers remain challenged by how to limit the impact of reducing liquidity and increasing interest rates. For some time now, market commentators and investment experts have been puzzled by the extended run of strong equity market returns. Developments through August continued to show that markets can be resilient, but that emerging concerns do require monitoring.

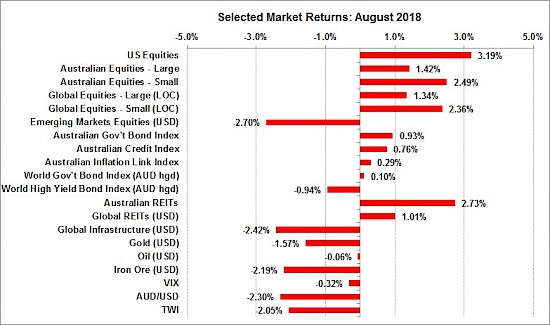

Geopolitical tensions, including new sanctions, trade tensions and inconsistent leadership are all being digested by markets, proving that it remains very difficult to predict short-term market movements (see August 2018 Market Returns chart); long-term, sensible investing and keeping key investment principles of diversification, lower turnover and seeking aligned investment managers are prudent philosophies to keep focused on.

Broadly, the US economy continued to show signs of economic strength, including higher quality economic growth, a very strong labour market and robust corporate earnings. European markets keep progressing in the right direction economically, with some key decisions to come in major economies like Italy through October as a new government comes into control. The Australian economy also looked to be in good shape with record low interest rates continuing to support business and capital investments. The RBA is specifically waiting for wage price pressures to arise before considering any change to interest rate policies.

Figure 1: All developed equity markets did well in August, outpacing an entire year of cash returns

Source: Thomson Reuters, Bloomberg 1 September 2018

USA

We’re seeing a gradual tightening of global liquidity as the US Federal Reserve moves its monetary policy settings back to “normal” levels. At this stage, the normalisation process looks like it has some way to go, which heightens the odds of more volatility in global markets. Emerging markets have been impacted the most, with pressure on currencies forcing leaders in these nations to take decisive action to protect currencies (specifically Argentina and Turkey).

Manufacturing activity is strong, the unemployment rate is low, and inflation has risen close to the Fed’s target. There is an ongoing debate about just how much more work the Fed needs to do with monetary policy. The Fed has outlined a path for gradually increasing interest rates from the current level of 1.7% to around 3.25% by early 2020. The markets think the Fed will be done with tightening by late 2019 with the cash rate around 2.75%. In a significant speech at the annual Jackson Hole Economic Policy Symposium, Fed Chair Jerome Powell emphasised that they would take a gradual approach to lifting interest rates and be guided by the economic data as it unfolds. The key point though, is that interest rates will continue to rise, and the Fed will continue to withdraw liquidity through its quantitative tightening program.

However, the impact of this is flowing around the world and some countries are less well positioned to deal with it than others. The most vulnerable nations are those which borrowed too heavily in cheap US dollar-denominated debt without taking the necessary economic reforms along the way. In some cases, this has been exacerbated by ineffective national governments and in many cases by the “trade war” rhetoric from the US administration.

Australia

In Australia, the tightening expectations for US interest rates and subsequent liquidity pressures, have led to out-of-cycle interest rate increases. This has been exacerbated by the increasingly stringent approach to lending that the banks have adopted in response to pressure from the Royal Commission and the regulators. Given all this, it is not surprising that house prices are now falling, and over-geared borrowers are starting to feel pressure; keep an eye out for resets of interest-only loans. Consumer confidence currently remains positive, however, a change of Prime Minister and households feeling some budget pressure may mean the Reserve Bank retains interest rates at record low levels for the foreseeable future.

Nevertheless, the local economy remains in good shape. Latest data shows business conditions and capital expenditure plans moderating from recent firmer levels, but GDP growth remains above trend and the unemployment rate has dipped further to 5.3%. Inflation remains at the bottom of the Reserve Bank’s target range and Governor Lowe has reiterated the likelihood that the cash rate will stay at 1.5% until there are meaningful signs of accelerating wage growth.

These are favourable conditions for the local bond and equity markets, with expectations of steady interest rates supporting the ASX 200’s Price/Earning valuation around current levels. The ructions in Canberra surrounding the change of Prime Minister produced some temporary volatility in our markets but with little lasting effect. Notably, the Australian dollar has continued to depreciate as US interest rates have risen above local interest rates and concerns about trade disputes triggered by the US have resurfaced. After many years of resilience, the so-called Aussie battler now seems destined for a sub $0.70 rate against the US benchmark.

International

The depreciation of our currency has been very modest compared with the experience of a number of emerging market nations who, like us, rely heavily on commodity exports. The pressure on these countries has been building all year and escalated significantly in August. Argentina and Turkey are particularly vulnerable and have increased interest rates sharply (to around 50% in Argentina and 20% in Turkey) in order to defend their currencies. This, of course, is very damaging to their economies and therefore equity markets have fallen sharply. Pressure is also building on India and Indonesia, both of which continued to lift interest rates through August.

In China, trade tensions escalating with the US is having an effect on Chinese output. Authorities there are trying to counteract these developments by reducing bank reserve requirements. Economic growth in the region continues to outpace all other major economies with the government strongly focused on continuing to keep the economy transitioning toward higher-quality growth and firmly entrenching the nation’s population in the middle to upper-middle class status. Their transition to the world’s tech centre also continues with a strong entrepreneurial spirit evident.

In conclusion

Overall, August economic data demonstrated that the global economy is growing above trend, a positive sign for companies and investors. Having said that, we remain prepared for ongoing geopolitical announcements as global leaders aim to prolong equity market strength while trying to push ahead with more “normal” policy measures as the lasting legacy of the GFC dissipates. We believe it’s prudent to be focused on the positives that equity markets can provide, with a firm stance on high market valuations and being prepared for the bouts of volatility that will inevitably arise by holding investments that can diversify equity market risk.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Paragem Pty Ltd [AFSL 297276] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at a personal level. No responsibility is accepted by Paragem or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.