Economic Snapshot: Central banks limited by COVID lockdowns

Summary

July saw markets continue to worry about the global growth outlook. Some key readings of economic activity in June were lower than in previous months, leading markets to revisit the “peak growth theme”. Potential disruption from the accelerating COVID waves around the world added to these concerns. This narrative outweighed some stronger than expected inflation figures. Some key central banks started talking about reducing Quantitative Easing (QE) programs, given economic data has been improving faster than expected. However, markets are not convinced the central banks can move as fast as they have said because of the impact of COVID lockdowns on economic activity. Regulatory change by Beijing caught markets by surprise towards the end of the month and knocked the Chinese equity markets back sharply.

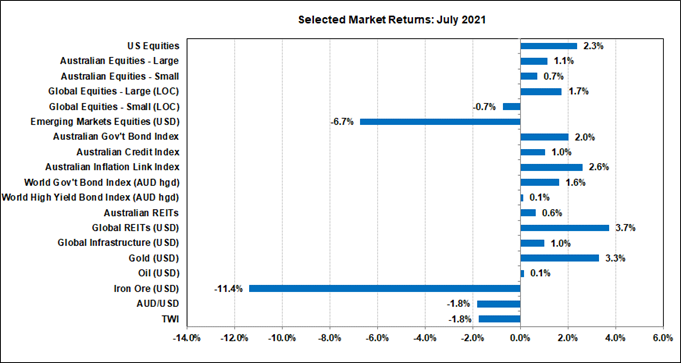

Government bond yields fell further as markets priced slower growth and extended easy monetary policy. The US 10 year Treasury Inflation-Protected Securities (TIPS) real yield fell to a new low of -1.16%. Equity markets performed well, with Australia, US and MSCI World equity indices making new highs. Concerns about peak growth and high valuations were offset by good earnings seasons and the prospect of ongoing monetary policy support. The Emerging Markets index was dragged down by weakness in the Chinese equity market.

The price of gold rallied as the number of COVID cases around the world increased and the US TIPS yield fell. A softer US$ also helped gold to rally. The A$/US$ slipped 1.8% in July to close at US$0.7381, the lowest level since early December 2020, on expectations of lower interest rates here than in the US.

Chart 1: Emerging equity index and iron ore fell sharply in July in response to developments in China

Source: Thomson Reuters, Bloomberg 1 August 2021

Coronavirus Pandemic

The delta variant of COVID has been spreading rapidly around the world. Here in Australia, the number of new cases per week has risen to nearly 1,500. While small compared with case numbers overseas, these are the largest figures we have seen since August 2020 when Australia was coming off its big second wave. Many other countries are seeing new COVID waves, including the US, parts of Europe, China, Japan and South Korea. On a more positive note, countries which were earliest into the delta wave, including the UK, Spain and Holland are now showing falling case numbers as the number of new cases per week appears to have peaked.

Australia

Latest domestic economic news shows Business Conditions in June slipping to 24.1 after 35.8 in May. Business Confidence also eased in June, however we need to remember that these figures are coming off record high levels and still represent a solid rate of growth for the economy. The labour market improved in June, with 29,100 new jobs and the unemployment rate falling to 4.9%. These figures show that conditions in the labour market continue to exceed the Reserve Bank’s expectations. The June quarter inflation figures showed headline inflation of 3.8% over the year to the quarter, but underlying inflation of only 1.6%, which is still below the Reserve Bank’s target of 2% - 3%.

Overall, these figures show our economy in a good light. Growth is respectable, unemployment is falling and the higher headline inflation figure was due to temporary factors. The Reserve Bank flagged it is thinking about scaling back its bond-buying program in view of these developments. However, the impact of the Sydney lockdown, which has now extended to other parts of the country, has led markets to believe the Reserve Bank will have to put these plans on hold, and may even have to temporarily expand its bond buying.

USA

A similar story applies to the US in July. Latest inflation (CPI) figures were somewhat higher than expected due to temporary factors, the forward-looking ISM Manufacturing PMI (purchasing managers index) slipped to 59.5 from 60.8, and the unemployment rate was 5.9% in June compared to 5.8% the previous month. Real GDP grew 6.5% over the year to the second quarter, compared with 6.3% over the year to the first quarter. The Federal Reserve again said it is discussing winding back its bond-buying program. Markets expect a more formal announcement in coming months.

Europe

In Europe, real GDP grew by 2% in the second quarter, well ahead of market expectations, the unemployment rate fell to 7.7%, and core inflation eased from 0.9% to 0.7% in June. The ECB announced it will continue to run an easy monetary policy for some time and will tolerate periods of inflation above 2%.

China

In China, GDP growth, which had been running a bit over 18% in year-on-year terms in quarter 1 (Q1), slipped to 7.9% in Q2. However, the Q1 figure was distorted by COVID-induced base effects from a year earlier. The quarterly rate of growth was actually a bit higher than expected. Late in the month Beijing announced crackdowns on education providers, property developers and tech companies. These moves are motivated by concerns about national security and social inequality. Markets were blind-sided by these developments and the share prices of affected companies fell sharply. Markets were already assessing prospects for slower growth in China and the impact of the new COVID wave appearing in parts of the country. In response to these concerns, Beijing announced more fiscal stimulus will be used to support the economy.

Bond & Equity Markets

In this environment, government bond yields fell further as markets priced slower growth and extended easy monetary policy. The Australian 10-year government yield fell 0.37% in July to end at 1.12%, the lowest level since January 2020. In the US, the equivalent bond yield fell 0.21% to 1.24%. Similar declines in yields were seen in European markets. The US 10 year TIPS real yield fell to a new historic low of -1.16%.

Equity markets performed well, with the Australian, US and MSCI World equity indices making new highs. Concerns about “peak growth” and high valuations were offset by good earnings seasons and the prospect of ongoing monetary policy support. The Emerging Markets index was dragged down by weakness in the Chinese equity market.

Gold Price & Exchange Rates

The price of gold rallied as the number of COVID cases around the world increased and the US TIPS yield fell. A softer US$ also helped gold to rally.

The A$/US$ slipped 1.8% in July to close at US$0.7381, the lowest level since early December 2020. The currency slipped as the Australia-US bond differential narrowed on expectations of easier monetary policy here than in the US

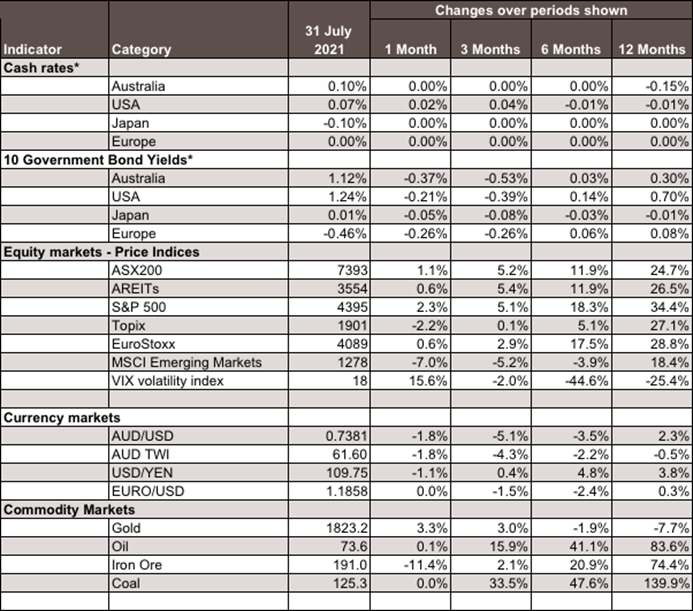

Chart 2: Major Market Indicators – July 2021

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.