Debt Recycling: a smart financial strategy

Purchasing a home can be one of life’s greatest milestones. Home ownership brings a sense of achievement and adds to your asset portfolio. A home is also likely to be your biggest purchase, and can subsequently become your biggest debt, often putting the brakes on your wealth accumulation. But what if you could build wealth tax-effectively and still pay down your home loan? That’s where debt recycling comes in.

Debt recycling is a strategy which allows you to convert non-tax deductible home loan debt into tax deductible investment debt. During this strategy, you pay down non-deductible home loan debt, and re-draw it as an investment loan to purchase a portfolio of investments which can grow, compound and tax effectively build your wealth. All additional income generated by your investments (e.g. dividends) is then directed to reducing your home loan.

This strategy is most applicable to higher income earners with an ability to pay down more than the minimum home loan repayments each month.

Consider a home loan of $500,000 with annual interest of 5% and principle and interest repayments of $60,000 p.a. After 1 year, the home loan would be paid down to approximately $465,000 and $35,000 can be re-drawn as a tax-deductible loan and invested into a portfolio of growth investments. The benefits of debt recycling compound over the long term and include a reduction in personal tax, paying down your home loan quicker, while building additional investment assets and an income stream.

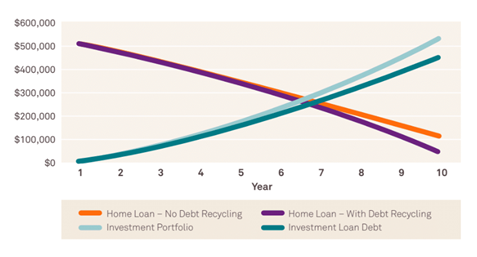

This chart shows debt recycling in action

On the other hand, you will still have debt (albeit deductible debt) and your level of risk is increased. Over time, the total amount of debt stays the same, but the nature of the debt changes, allowing more of it to become tax deductible each year, all while you are growing an investment portfolio for the future. Long term, as you repeat this process, your investment income and capital compound, and your non-deductible home loan debt can be paid off at a faster rate.

On the other hand, you will still have debt (albeit deductible debt) and your level of risk is increased. Over time, the total amount of debt stays the same, but the nature of the debt changes, allowing more of it to become tax deductible each year, all while you are growing an investment portfolio for the future. Long term, as you repeat this process, your investment income and capital compound, and your non-deductible home loan debt can be paid off at a faster rate.

Contact your adviser or book in for a free financial health check to find out if this strategy is right for you.

Note: The chart above assumes a starting home loan of $500,000 with principle and interest repayments of $60,000 p.a. being made at an interest rate of 5% p.a. Income earned from the investment portfolio is at a rate of 4.3% p.a. and this has been allocated toward the repayment of the home loan using this strategy. The investment portfolio has been assumed to grow by 3.59% p.a. Other factors such as higher interest rates and lower investment returns may alter this projection therefore it is important that you consult your FMD adviser to discuss whether this strategy is right for you.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.