4 things women can do now to enjoy a wealthier future

However rewarding our careers and growing families may be, most professional women also look forward to a future where they’ll have more time for themselves. Whether the goal is travel, a sea-change or just more time for fitness, study or long lunching with friends, making that future a reality takes money.

Alarmingly, new Australian research shows professional women are less likely to create the wealth they need to realise their financial goals. Despite being better educated and often earning high incomes (over 417,00 women earned taxable income above $100,000 in 2014-15 financial year) achieving financial success isn’t always a priority, even though an income advantage should mean a better lifestyle now and in the future.

The (HILDA) Survey which has tracked the lives of the same group of Australians over the last 17 years, recently asked participants to answer five questions (test yourself here) on topics such as inflation, portfolio diversification and risk versus return and the results showed a marked difference in the financial literacy and confidence of men and women. Half of the men answered the questions correctly compared with 35% of women.

This matters because we know those with lower financial literacy and confidence are less likely to use risk and return strategies to their advantage and less likely to seek professional advice to make the most of their high income producing years to create the lifestyle they want in the future. I’ve been advising successful professionals for 15 years and I know long-term financial well-being doesn’t happen by accident. You have to decide it’s important and find someone you trust to develop a plan to get you there.

While policymakers and employers need to do their bit to make super more equitable, women can take these proactive steps to take control of their financial future now:

1. Get to know your super or outsource it

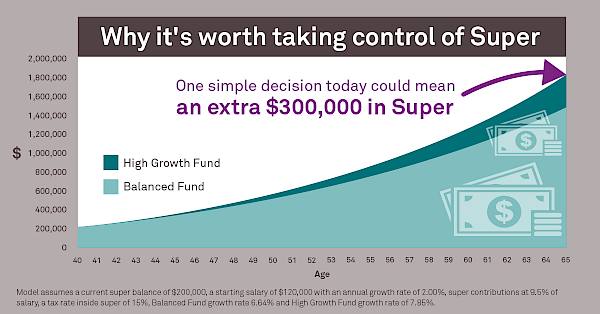

Superannuation is 9.5% of your salary so it’s important to actively engage with it. Get to know the fees and charges associated with your account, what your investment options are and how much insurance you have in super. You might find your risk appetite is growth-oriented but your super is invested in the default balanced option, robbing you of stronger potential returns.

Consider that for a minute, then look at the above chart. It shows how you could have an extra $300,000 in super by moving from a Balanced Fund to a High Growth Fund.

Maybe you have some insurance, but not enough to cover the mortgage if you are suddenly out of action with illness or injury. The successful, professional women I work with are busy people, so checking these details can fall off the to-do list, but they are vital to accumulating and protecting wealth.

2. Take control of your super contributions

Just $50 a week in extra super contributions will make a big difference to your super balance come retirement. Start making voluntary contributions to your super, and talk to your employer about salary sacrificing. Seek advice from a CFP®, CERTIFIED FINANCIAL PLANNER® to understand the tax implications and calculate your projected super balance under a range of different contribution scenarios.

3. Set a realistic goal that works for you

Understand the fundamentals of a self-funded retirement and assess your finances as part of a bigger picture. Having a goal is key, but avoid chasing an arbitrary target - like the commonly touted $1million comfortable retirement. In reality, it comes down to understanding where you are now, where you want to be, and designing a superannuation roadmap that will guide you towards that future.

4. Find a professional financial adviser you like and trust

According to research by Roy Morgan, in the 12 months to December 2017, only 11.3% of women sought professional advice around their super1. Australia’s superannuation is a complex and evolving system. It is difficult and time-consuming to stay on top of all the changes, and there’s no reason to go it alone. Find an FPA-certified professional practice so that you can be assured of tailored advice that has your best interests at heart.

Superannuation is an extremely tax-effective way to build wealth. Taking control of your super today means you won’t need to rely on anyone else to have the quality of life you deserve in retirement.

Take the next step in maximizing your super and get a free financial health check

How a financial adviser can help

• Financial education: An adviser can help you get comfortable with understanding the various superannuation and investment terminologies – it will make discussing your options a lot less daunting.

• Customised plan of action: Your adviser can help you develop a financial plan and keep you on track to achieving your super goals through tax-effective strategies that are aligned with your circumstances and risk profile.

• Administration and reporting: The onerous reporting requirements associated with managing an SMSF are time-consuming and require expertise. A financial adviser will take care of this for you.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.