Economic Snapshot: Markets face headwinds

The Reserve Bank of Australia (RBA) chose not to lift rates at the September and October meetings, giving itself more time to assess the impact of the four percentage points of interest rate hikes delivered since May 2022.

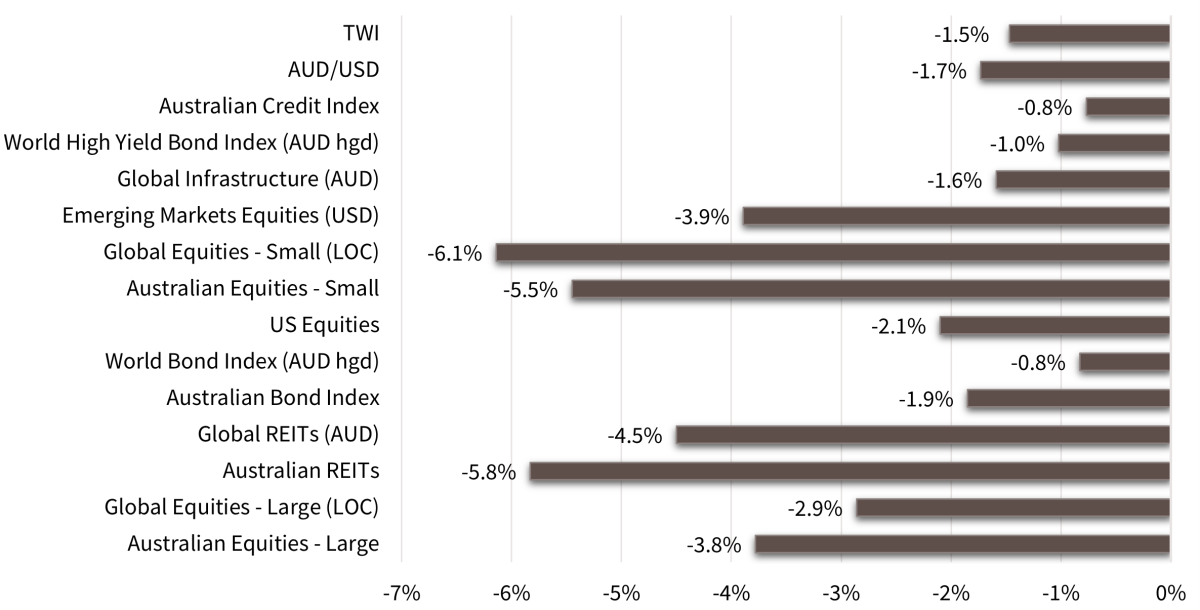

Global equity markets dropped a further 2.9% in October taking the year-to-date return to 8.2%. Bond yields continued to climb, undermining valuations across a range of assets, while the Israel-Hamas conflict added to uncertainty and risk aversion.

The Australian equity market lost 3.8% in the month and is now down marginally for the year to date. Healthcare stocks sold down 7.1%, while financials and REITs were down 3.7% and 5.7% respectively.

Global bond yields continued their march higher in October, against the backdrop of a more resilient economy. Australian bond yields sold off more aggressively than their US and global counterparts, as markets priced in another RBA tightening in November following the higher-than-expected September quarter CPI (inflation) result.

Asset Class Returns - October 2023

Source: Zenith Investment Partners Pty Ltd, Monthly Market Report, Issue 116, September 2023

Global Developed Equities

In October, global equity markets declined by 2.9%, bringing the year-to-date return to 8.2%. Bond yields rose, affecting valuations, and the Israel-Hamas conflict added uncertainty.

US bond yields reached 5%, causing a “bear market flattening”. Earnings exceeded expectations, particularly in communication services, consumer discretionary, and financials, with the consensus predicting over 10% growth for the next year.

The Israel-Hamas conflict initially impacted markets but as it didn’t escalate to a broader regional conflict it has not yet had a sustained impact. However, the situation remains fluid.

The Bank of Japan (BoJ) moved toward ending Yield Curve Control and exiting negative interest rate policies. Although they refrained from totally abandoning the program, BoJ did relax the “cap” on 10-year yields. However, Japanese rates remain well below global rates.

Despite a decline in inflation, the resilient global economy reduced expectations for easing in 2024 and 2025. The US outperformed major regions, while Italy and Denmark led for the year, and Hong Kong, New Zealand, and Israel lagged.

Quality stocks outperformed, down 1.7%, while Value stocks lagged at 3.4%. IT and communications services were up, while healthcare and banks declined for the year.

Australian Equities

In the last month, the Australian stock market fell by 3.8%, making it slightly negative for the year. As was the case with global trends, the market faced challenges from higher bond yields and reduced price-to-earnings ratios.

However, the outlook for Australian company earnings is weak, with the market anticipating a 1% fall in growth in earnings per share for the next 12 months across the market.

Healthcare stocks experienced a 7.1% decline, contributing to a 14.7% decrease in 2023. Financials dropped by 3.7%, and Real Estate Investment Trusts (REITs) fell by 5.7%, largely due to increased real bond yields.

A recent NAB economic survey indicated that business conditions, while softer, remain above average. Despite slightly softened job growth statistics, the labour market is still tight.

Inflation concerns led to market expectations of another rate hike by November, following a higher-than-expected September quarter Consumer Price Index (CPI) showing 1.2% inflation.

The Reserve Bank of Australia (RBA) chose not to raise rates in September and October, allowing time to assess the impact of the previous 4% interest rate hikes since May 2022.

Market pricing implied a high probability of another rate hike to 4.35%, subsequently delivered, with the possibility of another by June 2024.

Emerging Markets

Emerging markets declined by 3.9% in USD terms in October, bringing the year-to-date performance to a 2.1% decrease, trailing global developed equities by approximately 10%.

The Chinese equity market faced challenges due to a weak property market and limited policy response, resulting in a 4.3% drop for the month and an 11.2% decline for the year.

China's economic data showed a better-than-expected 4.9% GDP expansion in Q3 and stronger retail sales, but October PMI readings fell below the critical expand/decline level of 50 suggesting the manufacturing sector remained sluggish.

Other regions were all largely weaker with the MSCI Asia index down ~4% and Latin American falling by 4.8%.

While emerging markets appear inexpensive compared to developed markets, a catalyst such as rate cuts from the Federal Reserve or additional Chinese stimulus, may be needed for sustained outperformance.

Property and Infrastructure

In September and October, rising real yields negatively impacted infrastructure and REITs. Despite REITs already factoring in property value declines, a 65-basis point increase in real yields led to a 5.8% decline in October, adding to the 8.6% drop in September.

Year-to-date, REITs are down 5%. Global REITs also fell by 4.5%, totalling an 8.6% loss for the year.

Global infrastructure declined by 1.6% in October, following losses of 4.2% in September and 4.7% in August, influenced by a 100-basis point rise in US 10-year Treasury Inflation Protected Securities (TIPs) yields since July.

Fixed Interest – Global

Global bond yields continued to rise in October, with the US 10-year yield reaching 4.88%, up more than 120 basis points since June.

The Barclays Global Aggregate (AUD hedged) index declined 0.8% in October and nearly 15% since the end of 2020. Despite a resilient US economy growing at a 4.9% annualized pace in Q3, higher inflation, a growing fiscal deficit, and increased treasury issuance led to rising yields.

The term premium, the reward for holding long-term fixed returns, increased from -0.75% in June to 0.5%.

The Bank of Japan moved closer to ending Yield Curve Control, acknowledging its untenable defence of the 1% Japanese cash rate.

In Europe, with inflation at 2.9%, the ECB is expected to maintain steady rates. US credit spreads widened to 442 basis points, raising concerns over corporate refinancing risks, but attractive yields make the corporate bond sector appealing to income investors that understand these risks.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.