Economic Snapshot: Global markets deliver a reality check

After a positive start to the year in January, global investors faced a reality check in February.

Bond and equity markets gave up some of their earlier gains as questions were raised about the prospects for economies and interest rates in the coming year. A slew of stronger than expected growth and inflation data led markets to re-price their expectations about interest rates to reflect a more cautious view of what central banks are likely to do.

The degree of uncertainty among investors about how this year will play out is noticeably higher than usual. Everyone knows there are lags involved in monetary policy impacting the economy, but recent data in the US really have muddied the waters.

Discussion about whether there will be a soft landing or a hard landing has been supplemented by the possibility of no landing. Wonderful though that would be, it seems to fly in the face of the need to generate some spare capacity in the economy to ensure inflation stays down.

At the moment, equities and credit markets seem to be favouring the soft/no landing outcomes. The pricing of these assets does not appear consistent with economies slowing enough to lift unemployment rates. The picture will become clearer as the year unfolds, but it seems highly likely we will see more volatility in the meantime.

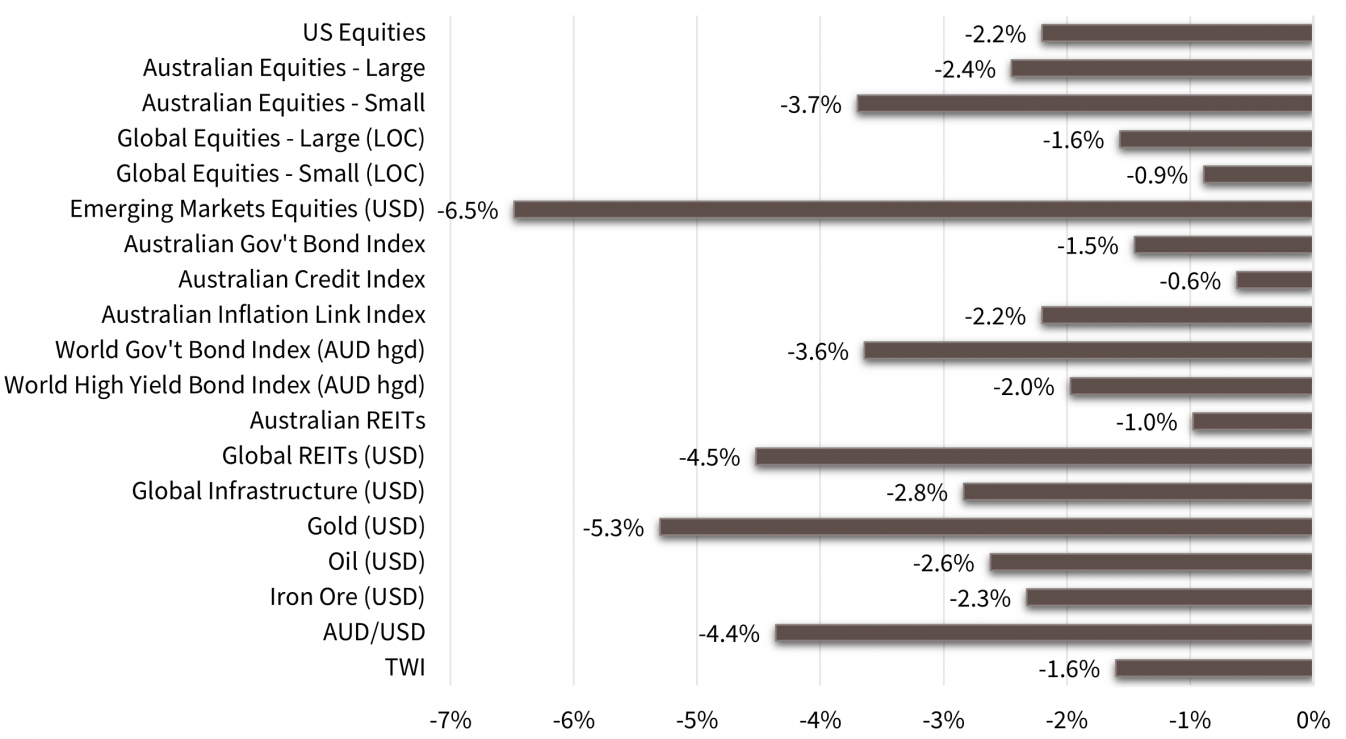

Chart 1: Renewed concern about interest rates tipped bond and equity markets into losses in February.

Source: Thomson Reuters, Bloomberg, 1 March 2023

Financial Markets

After a positive start to the year in January, global investors faced a reality check in February.

Bond and equity markets gave up some of their earlier gains as questions were raised about the prospects for economies and interest rates in the coming year. A slew of stronger than expected growth and inflation data led markets to re-price their expectations about interest rates to reflect a more cautious view of what central banks are likely to do.

Economic Indicators

The US labour market report released at the start of the month set the tone. Investors were astonished to see the US economy added 517,000 new jobs in January and that the unemployment rate fell further to 3.4%.

The increase in employment was way more than what the markets had been expecting. Similarly, the latest data on job openings and hires showed the excess demand for labour increasing rather than falling, as the Fed wants to see. Furthermore, although the ISM manufacturing activity index fell in January, the corresponding services index rose sharply back to where it was in October/November.

After some of the most aggressive interest rate rises seen in a long time, markets are expecting to see evidence of the economy slowing down. While there has been some data confirming that, the labour market and services data, along with figures on retail sales and housing, were strong enough to make the markets start to question the slowing narrative and wonder how much more work the Fed has to do to cool the economy enough to get inflation under control again.

Inflation

As it turned out, the latest US inflation data were less encouraging than the markets had hoped. Headline CPI inflation rose 0.5% in January – the highest monthly increase since June 2022 – and 6.35% over the year to January. Core CPI inflation rose 5.55% over the year to January, which was slightly slower than for the preceding month. However, core services inflation accelerated a bit to 7.16% over the year. The key core PCE deflator measure that the Fed uses was 4.71% over the year to January compared with 4.6% the month before.

Bond Yields

In the face of all this, it was not surprising that Fed officials made hawkish comments about the need for further rate hikes and their resolve to tame inflation.

By the end of the month, markets had revised up their estimates of the peak of the Fed funds rate to 5.4%, compared with 4.9% a month ago. That in turn flowed through to other assets, with the US 10-year bond yield rising 0.4% and moves of similar magnitude in several other countries. Here in Australia, our 10-year bond yield rose 0.3% to close the month at 3.85%.

Real bond yields also rose, with the US 10-year TIPS yield climbing back to 1.5%. Inflation expectations moved up to around 2.5%, which is still reasonably benign and does not suggest the bond market is losing confidence in the Fed. However, higher real yields undermine equity market valuations and prospects for higher interest rates undermines sentiment about company earnings growth.

Equity markets responded by giving up some of January’s gains, though the declines were generally moderate. Emerging market equities were an exception, falling 6.5% in February, as the US$ rose with higher expected interest rates. Similarly, the A$ fell over 4% given the stronger US$, finishing the month at US$ 0.673 compared with US$ 0.704 at the end of January. The price of gold also fell because of the US$ and interest rates story.

Australia

Latest data for our economy showed some improvement in business conditions, confidence, and employment intentions in January. However, consumer confidence slipped again in February after some improvement in January.

The labour market saw a small fall in employment and a slight increase in the unemployment rate to 3.7%. The wages index rose 0.8% in the December quarter and 3.3% over the year to the quarter.

This was the largest annual rate of wage increase since late 2012. Like their Fed counterparts, Reserve Bank officials reiterated their resolve to curb inflation and flagged that will involve more interest rate increases. The market is now pricing a peak cash rate around 4.3%, compared with 3.75% a month ago. The market does not expect the Reserve Bank to start cutting the cash rate until Q2 2024.

Outlook

The degree of uncertainty among investors about how all these crosscurrents will play out this year is noticeably higher than usual.

Everyone knows there are lags involved in monetary policy impacting the economy, but recent data in the US really have muddied the waters. Discussion about whether there will be a soft landing, or a hard landing has been supplemented by the possibility of no landing. That is, economies, including the US and Australia, can continue to grow without recession while inflation benignly declines.

Wonderful though that would be, it seems to fly in the face of the need to generate some spare capacity in the economy to ensure inflation stays down. Just as interest rates had reached unsustainably low levels, so capacity use had reached unsustainably high levels. Central banks are committed to rectifying both these imbalances to put economies on a more sustainable path in the years ahead.

Now, equities and credit markets seem to be favouring the soft/no landing outcomes. The pricing of these assets does not appear consistent with economies slowing enough to lift unemployment rates. The picture will become clearer as the year unfolds, but it seems highly likely we will see more volatility before the year is over.

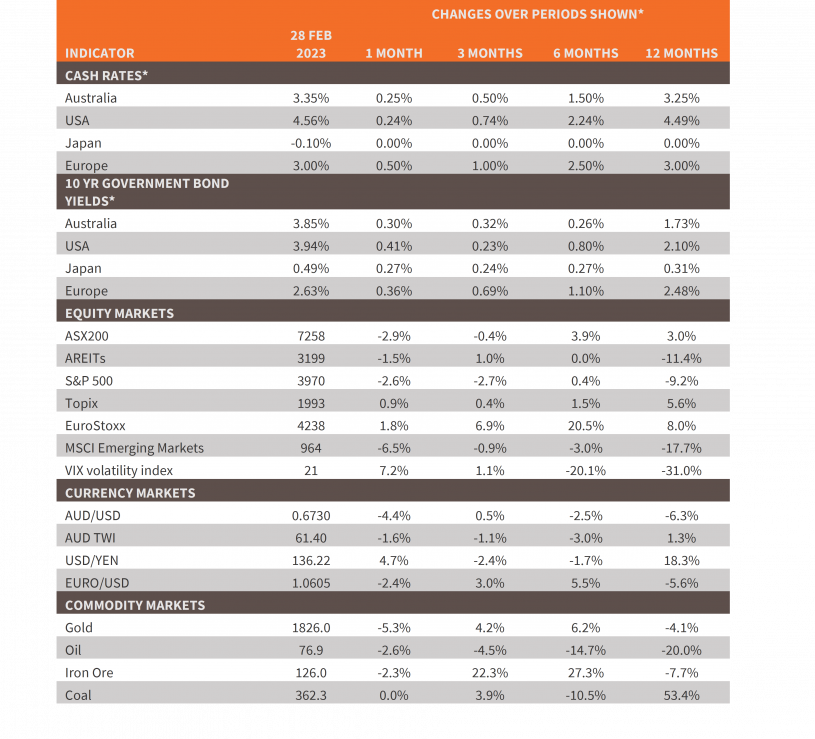

Chart 2: Major Market Indicators – February 2023

*For cash rates and bonds, the changes are percentage differences; for the rest of the table percentage changes are used.

Disclaimer: This document has been prepared for the FMD Financial Economic Snapshot by Caravel Consulting Services Pty Ltd [AFSL 320842] and is intended to be a general overview of the subject matter. The document is not intended to be comprehensive and should not be relied upon as such. We have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained in this document. Advice is required before any content can be applied at personal level. No responsibility is accepted by Caravel Consulting or its officers.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.